Disclaimer: This isn’t Funding recommendation. PLEASE DO YOUR OWN RESEARCH !!

Abstract:

For those who would ask me about essentially the most boring inventory of my typically very boring portfolio, I may identify Schaffner Group. I had purchased a primary place again in 2021 throughout my “All Swiss Shares” collection.

Nevertheless, I’ve by no means written a extra detailed write-up despit my annual summaries (2021/2022 , 2022/2023), possibly becasue I at all times bought bored once I began writing about it ? Over time I added to the place and after the newest 6 months numbers, I made a decision to extend right into a full place. Time to elucidate the funding case a little bit bit higher.

- The Firm – Transformation

Schaffner Group is a Swiss firm that underwent a major tranformation over the previous few years. Most significantly, they managed to dispose their second largest division “Energy Magnetics” which was loss making in 2021 and deal with 2 divisions: EMI Filters and Automotive. That is how Schaffner describes their tranformation in a 2022 investor presentation:

For some causes, the final 2 years nonetheless have been “noisy”. In 2020/2021 (Monetary 12 months goes from 01.04 to 31.3.), they needed to ebook a (non money) loss for the ability magenitics disposal, in 2021/2022, the Automotive division suffered from the provision chain points within the car business.

Nevertheless, below this noise, the core division, EMI filters grew steadily. Now, in FY 2022/2023, with a sure restoration of the Automotive section, the true high quality of the enterprise begins to emerge. However extra on this laters.

2. The enterprise & Merchandise

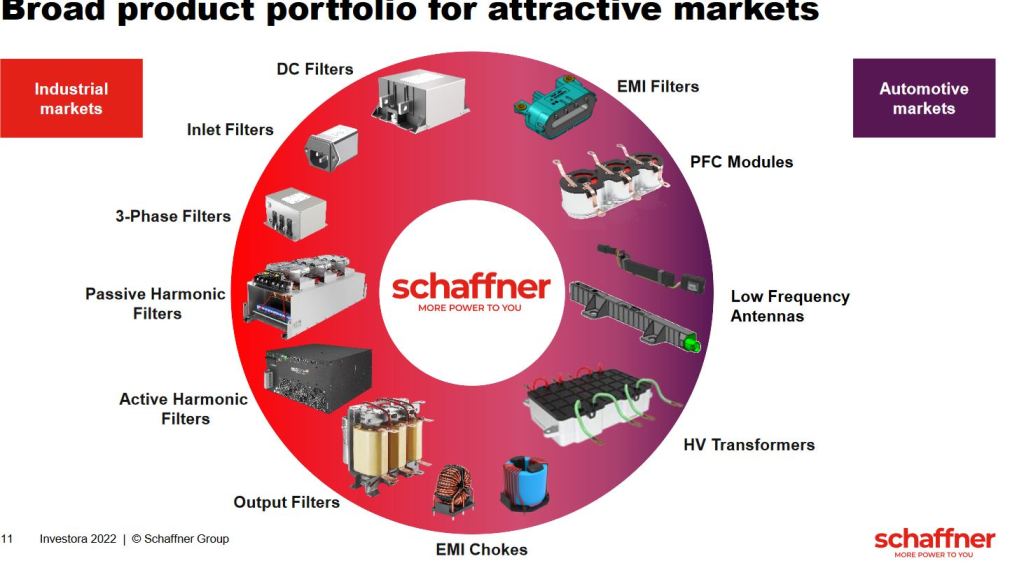

Schaffner has a pleasant graph in one in every of theri presentation how their merchandise seem like:

These merchandise at first sight are clearly not “horny client” merchandise that you simply discover within the grocery store however fairly small, however essential components for different producers (B2B).

The primary product line of Schaffner are EMI Filters. Yow will discover an in depth description of those Filters and why they’re wanted for example right here. In a nutshell, {most electrical} equipement requires these filters with a purpose to forestall electro magnetic interference (EMI) between completely different digital circuits. Though these elements are usually comparatively low worth objects, they normally should be customized made to immediately match the particular objective and there are sometimes business norms that require the usage of these filters.

It appears to be that it is a small however rising business with only some gamers and Schaffner appears to have a world market share of round 20-30%. So on this small pond, it’s a fairly huge fish.

Schaffner’s enterprise mannequin is to largely desgin the elements in Switzerland however manufacture them in China and Thailand, in order that they appear to be very competitve on value.

What I discover most attention-grabbing is the actual fact, that there’s structural progress on this business because the elevated electrification means structurally increased calls for for his or her elements. EV charging, semi-conductor manufacturing and heatpumps are just a few areas that Schaffner mentios that presently drive progress and can so for the foreseeable future.

3. How have issues progressed ?

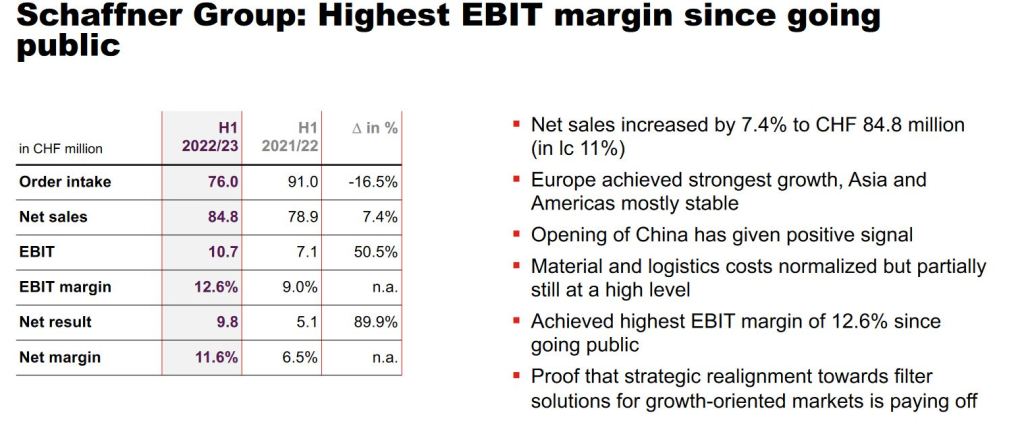

Since I’ve purchased the primary shares, the Industrial division has grown steadily, however as talked about, the Automotive division had some issues. Within the curren monetary 12 months nonetheless issues look good and Schaffner, which communicates usually fairly undertsated bought nearly euphoric:

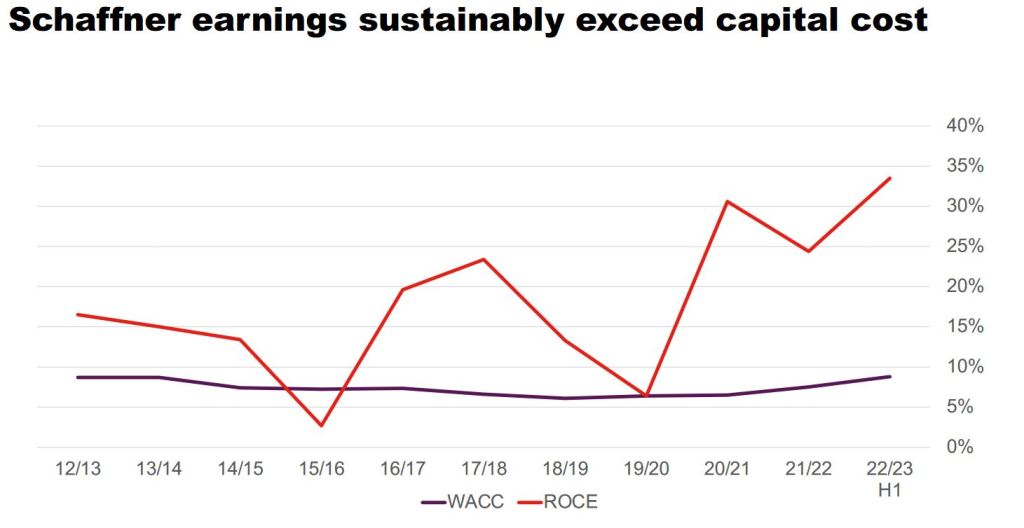

Schaffner had intitially guided mid time period goal of an EBIT-Margin of 10-12% and an natural progress charge of 5% p.a., each targets have been surpassed and so they appear to be fairly optimistic for the complete 12 months. That is supported by a really capital environment friendly bsuiness mannequin with reaching 33% ROCE within the first 6M:

4. Valuation

With 631‚069 excellent shares and a share value of 285 mn CHF, the corporate is valued at ~180 mn CHF. Schaffner has round 8 mn in web money at 31.03 so this interprets, if we simply double 6M numbers. into an anticipated P/E of 9,2x and EV/EBIT of 8,0 for the present 12 months. Not unhealthy for a double digit EBIT margin enterprise with a excessive ROCE and a very good probability of respectable progress and a rock stable steadiness sheet. Particularly when considerung {that a} regular Siwss enterprise with this KPIs would simply commerce 50% or costlier.

5. Why is the inventory low-cost ?

I feel there are just a few apparent causes, the primary being a really weak long run observe file which is mirrored in an extremly unispiring long run share value:

Schaffner at the moment is buying and selling under its IPO value of 1998 and has oscillated between 100 and 300 CHF for the final 15 years or so. So clearly, buyers don’t appear to be satisfied but, that Schaffner will likely be on a long run success path.

As well as, the final 2 years have been noisy and just one analyst appears to cowl Schaffner. Liquidity is simply modest, it’s not simple for a fund or bigger investor to get out and in shortly. Schaffner additionally experiences solely twice a 12 months and doesn’t present quarterly updates. Not everybody likes this, i do.

Schaffner additionally has some China publicity and appears to make use of round 300 folks in China. The bigger manufacturing hub nonetheless appears to be Thailand with 1000 workers.

Final however not least, the enterprise mannequin at first sight isn’t very horny and in addition not simple to grasp.

6. Administration, shareholder construction, different stuff

The biggest investor is a monetary investor known as BURU Holding who additionally owns a 20% stake in Kardex, one other top quality Swiss producer. BURU Holing is run by Philipp Buhofer, a Swiss Investor who appears to play the lengthy sport and appears to be fairly lively. Marc Buhofer, clearly a relative, owns one other 3% of Schaffner.

CEO Aeschliman was appointed in 2017. He owns round 2100 shares which is a little bit bit lower than his annual wage, however quantity is rising on account of incentive applications. The incentives are based mostly on EBIT margins, free cashflow and particular person targets, General I might charge the mixture of shareholder & Managment pretty much as good.

As talked about above, steadiness sheet high quality is excessive, with 8 mn web money and no goodwill.

Capital allocation is comparatively clear: They pay out round 40-50% of the revenue in dividends and the remaining will go in the direction of selective M&A.

Perhaps one comment with regard to a possible catalyst: I feel there may be none or solely a really small one. The one potential “tender catalyst” may very well be a potetnial dividend improve. In the event that they keep on with their 40-50% pay out rule, 40% of a possible 20 mn web revenue in 2022/2023 could be round 12,50 CHF per share, a major improve in comparison with the 9 CHF paid in for the earlier 12 months.

Abstract:

The general case for Schaffner might be summarized fairly simply: One can get a very good firm with an excellent enterprise at a wonderful value.

The mix of a double digit EBIT margin (12%) , double digit natural progress, ROCE within the 20-30% and a valuation of ~9x 2023 P/,E for me is a good wager on the expectation, that the way forward for Schaffner appears higher than the previous.

For me, Schaffner is without doubt one of the most attention-grabbing circumstances of a standard enterprise that may doubtlessly profit from a protracted progress development in the direction of electrification. Sure, it’s a trunaround, however in contrast for example to Meier & Tobler on the time of the funding, the flip round has already occurred and so they now “solely” have to proof that this was not a one-off.

Even when this journey is bumpy, I feel over the subsequent 3-4 years, the shares may supply a good return. On high of an anticipated dividend yield of as much as 5% p.a. I may simply think about one other 10% pa. as a mix of progress and a slight a number of growth kind the present low ranges. In the perfect case, this might even develop into a “Meier & Tobler 2.0” if the inventory trades at “Swiss High quality multiples”.

I’ve subsequently elevated the place additional to a 6% weight and financed this largely via an extra lower in Meier & tobler which is no longer so low-cost anymore.

One ought to point out that the share isn’t overly liquid, on common, 300-400 shares are traded each day on the Swiss change.

{kind=link}