In case you’re an present house owner who bought your property as lately as 2022, you most likely have a extremely low, fastened mortgage charge. Maybe one thing that begins with a 2, 3, or 4.

In spite of everything, mortgage charges hit document lows in 2021 and have been usually very low-cost for a couple of decade.

In spring of 2022, that modified and charges started surging larger as inflation took maintain and the Fed ended its MBS-buying program often called Quantitative Easing (QE).

Whereas 30-year fastened mortgage charges are now not a screaming discount, they’re not removed from their long-term common of about 7.75%.

However as a result of every thing else is so costly, the mortgage itself truly eats up a smaller share of whole housing prices.

Housing Prices Go Far Past a Easy Mortgage

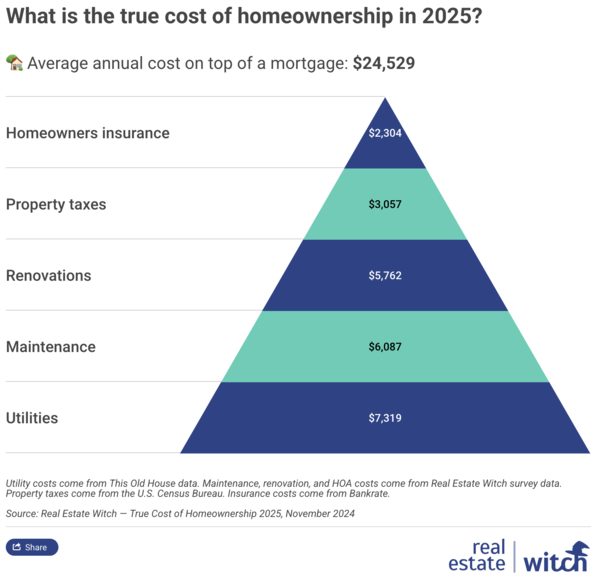

A brand new survey from Actual Property Witch discovered that non-mortgage prices have elevated to $24,529 for 2025, up from $17,958 in 2024.

This consists of owners insurance coverage, property taxes, dwelling renovations, routine upkeep, and month-to-month utilities.

Damaged down it seems like this:

Utilities: $7,319

Upkeep: $6,087

Renovations: $5,762

Property taxes: $3,057

Owners insurance coverage: $2,304

Relying on the place you reside, a few of these prices may appear low or excessive, but it surely’s the typical price taken from varied web sites utilized for the survey.

And chances are high owners insurance coverage will solely be going up subsequent yr, just about regardless of the place you reside.

In the meantime, the standard family spends $26,508 yearly on the mortgage, which isn’t way more than these different prices mixed.

In different phrases, the mortgage now solely makes up about half of the overall annual housing expense.

If we embody of us who dwell in owners associations, the non-mortgage whole rises to $27,606 yearly, which is above the standard mortgage expense.

That is one thing to contemplate in case you’re weighing a hire vs. purchase determination and focusing solely on mortgage charges and residential costs.

Make sure you think about all the opposite prices, each anticipated and sudden, while you make this dedication.

The survey additionally revealed that roughly 8 in 10 owners (81%) stated the “true price of proudly owning a house” was larger than they anticipated.

In the meantime, nearly half (44%) stated they felt it’s simpler to be a renter than a home-owner.

We’re All Paying for These Report Low Mortgage Charges Not directly

These days, the mortgage has develop into one of many least expensive elements of homeownership, whereas all the opposite prices have develop into costlier.

That is fairly distinctive, and it’s seemingly due to these document low mortgage charges, which sarcastically could be accountable for the following inflation we’ve skilled recently.

You see, all these years of straightforward cash and low rates of interest had a value. And that value is inflation, with the greenback eroding in worth as the price of nearly every thing has risen tremendously.

Nevertheless, the fortunate owners who have been capable of lock in a 30-year fastened at 2-4% have an unbelievable inflation hedge.

However you may argue that they’re paying for it one other method now, through rising prices elsewhere.

And it’s even worse for individuals who have but to enter the housing market, who’re dealing with the worst affordability in many years.

Renters are coping with larger prices throughout the board resulting from all that inflation, which may partially be blamed on the zero rate of interest coverage (ZIRP) put in place post-2008 and once more in the course of the pandemic.

Nevertheless, they’re receiving not one of the profit, in contrast to owners.

In the meantime, there are the house consumers who needed to accept a mortgage charge within the 6-8% vary over the previous couple years due to stated inflation.

All the things has a value, and in the end this creates a fair larger divide between the haves and have nots.

As soon as You’re Free and Clear You Nonetheless Gained’t Be Actually Free as a House owner

This brings up one other essential level. Say you repay your mortgage in full. Lots of people have been large on paying off the mortgage early recently.

Whereas I don’t agree with it, assuming you may have an excellent low fastened charge (which I see nearly as good debt), it doesn’t imply you’re with out funds.

As illustrated above, you’re nonetheless on the hook for property taxes, owners insurance coverage, upkeep, utilities, and renovations if crucial.

And that may quantity to some huge cash, even in case you now not have a mortgage.

So one has to query if free and clear truly lives as much as its identify. Certain, it’s one much less invoice, but it surely doesn’t imply you’re dwelling without spending a dime!

Lengthy story quick, in case you’re considering of shopping for a house, remember to use a superb mortgage calculator that components in ALL the month-to-month prices.

And don’t underestimate something. If something, overestimate to depart room in case these prices proceed to rise. They seemingly will!

In any other case, you could be just like the almost 1 in 4 millennial owners (23%) who stated the prices of homeownership have made them need to return to renting.

The survey, carried out between November twenty seventh and thirtieth, 2024, requested 1,000 American owners about their homeownership-related bills and their experiences coping with these prices.

(photograph: atramos)

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) dwelling consumers higher navigate the house mortgage course of. Comply with me on Twitter for decent takes.

{kind=link}