Disclaimer: This isn’t funding recommendation. PLEASE DO YOUR OWN RESEARCH !!!!!

As talked about within the Efficiency assessment, I had already construct up a brand new place in late 2024 in a brand new inventory. This time I’ll attempt one thing new: I’ll solely put up just a few sections of the write-up and solely those that ship me an e mail will obtain the complete model (without cost after all).. The rationale for that is that I’m actually how most of the readers are actally studying the complete doc. The bonus music after all is included on this put up on the finish.

0. Funding meme

For some unusual cause, I felt the urge to start out the pitch with this quite “German humor” meme:

- Elevator pitch:

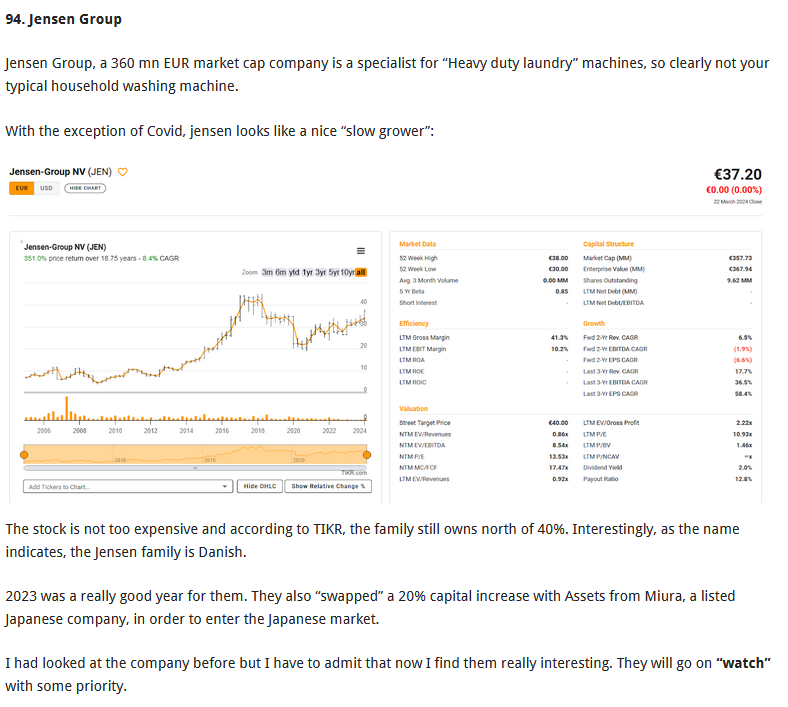

Jensen-Group, an organization initially from Denmark, now listed in Belgium, is a 420 mn EUR market cap “hidden champion” that’s the world market chief in “Heavy laundry” tools and automation. The corporate is run in third era by the Jensen household which nonetheless controls 40% of the shares.

The corporate manufactures and sells globally and is using some structural tailwinds, most notable power/useful resource effectivity and automation.

After a Covid pushed hunch in gross sales, 2023 revenues and earnings have surpassed pre-Covid ranges by a big quantity and 2024 seems to be like one other double digit development 12 months (gross sales +10%, EBIT +20% 9M 2024).

The corporate now achieves stable double digit EBIT margins (11,4% EBIT margin YTD) and a ROCE >20%. Though the inventory worth is near ATH (and the inventory is up +30% over 1 12 months), the valuation may be very low with a P/E of round 10x for 2024 (and nearly no debt).

Though there isn’t a “arduous” catalyst, I do suppose that the inventory is a doubtlessly very engaging funding at present worth ranges for the affected person enterprise targeted investor.

- Introduction:

I had put Jensen Group on my watch checklist throughout my “all Belgian Shares” collection in April and now its time to actually comply with on. That is what I had written again then:

- The corporate

3.1. Historical past

Jensen was based in 1937 in Denmark and is presently led by Jesper Munch Jensen in third era. The corporate has a really good historical past web page. In a nutshell, the corporate really began as a dairy restore store however then moved into laundry know-how and thru acquisitions and personal developments turned a number one provider of huge scale laundry options.

3.2. KPI overview

3.3. What Downside does Jensen Group remedy ?

Jensen is a equipment manufacturing firm that gives options for “heavy responsibility” wet-laundry functions. On their web site they provide a very good overview of their utility areas:

So Lodges, Hospitals. Cruise Ships are all heavy customers of “heavy responsibility laundry”. Regardless of the standard of the laundry course of itself, workers scarcity appears to be an enormous difficulty within the laundry business as nicely.

One must type the soiled laundry, deal with it and in the long run dry and fold it and never combine laundry items throughout batches. Up to now, to my understanding, there was a excessive degree of guide work concerned which appears to develop into increasingly troublesome to fill.

What Jensen Group gives are kind of absolutely automated options for a lot of the heavy responsibility laundry course of that may run 24/7 with a really diminished requirement of guide labour.

In case you need to study extra, Jensen has a number of good Youtube movies displaying completely different merchandise and laundry factories. I discover these Movies fairly enjoyable after a tough day 😉

Compared to most opponents, Jensen can construct a big “laundry manufacturing unit” fully and wherever on the planet resulting from their international presence.

6. Valuation / Anticipated return

Within the first 9 months of 2024, Jensen reported fairly spectacular numbers:

EBIT margins have additional elevated from 10% in 2023 to 11,5%.

Sadly, they don’t escape natural development (Maxi Press is included on this)however nonetheless this seems to be spectacular. Particularly the numerous order consumption appears to point that additional development may be on the horizon.

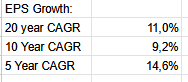

Traditionally, Jensen has grown EPS by 11% over 20 years. Within the final 5 years, together with the Covid interval, development accelerated to ~15% p.a.

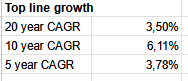

Gross sales development has been considerably decrease and appears like this (till 2023)

This hole is defined by way of a big improve in profitability particularly on the backside line from 0,6% in 2003 to 7,8% in 2023.

So the problem right here is clearly to give you a practical development price for Jenesen going ahead. It’s also clear that the final 2 or 3 years are usually not consultant with respect to high line development.

Alternatively, as talked about earlier than, there are some robust elementary tailwinds for Jensen. As well as, there’s additionally a very good probability to promote larger worth parts (Robotics, Software program) and growing the share of Companies is a transparent technique, supported by the acquisition of Maxi Press.

Personally, I feel an natural EPS development price in a spread of 5-10% just isn’t completely unrealistic for the subsequent 2-5 years.

One attention-grabbing side with regard to quick time period development can also be the very fact, that the massive business truthful TEXCare, which often takes place very 4 years occurred in November 2024. Apparently, the TEXCare 2020 didn’t occur resulting from Covid so this was the primary huge truthful after 8 years. I learn a number of feedback that the business was VERY proud of orders at teh fare. I’m actually wanting ahead what Jensen will say once they report 2024 quantity s in early March.

It must be seen how Money conversion seems to be in a extra “regular” 12 months like 2024. if we assume a 80% conversion, then based mostly on ~50 mn EBIT for 2024, FCF could be~ 40 mn EUR and(together with Maxipress buy worth) someplace between 7-9% present FCF/EV yield.

That in flip would lead to a return expectation in a spread of 12-19% p.a. plus any further return from a a number of growth.

As Jensen pays out solely a relative small portion of that money in Dividends plus some share purchase backs, the massive query after all is how they are going to allocate money going ahead. For my part, they’ve allotted capital very nicely up to now and I see no cause why this could change anytime quickly.

There are additionally not a number of comparable firms that I can consider, definitely in a roundabout way. From my present universe, I might suppose Krones and 2G Power may be the closest ones that I can consider. Each promote globally, assemble relativ advanced machines and don’t promote to vehicle producers.

Here’s a small comp sheet:

We will see that Krones, the bigger German producer of bottling machines is equally valued, 2G a lot larger. Krones as such can also be an attention-grabbing firm that I need to look deeper, similar as 2G. Nevertheless, in 2G’s case, a number of development appears to be priced in.

10. Conclusion & Abstract:

As talked about to start with, it took a while earlier than my enthusiasm grew for the corporate. I had appeared on the firm already just a few occasions till I obtained actually . Nevertheless, the extra I researched and examine them, the higher I appreciated the corporate and the enterprise.

On the backside line, one will get a decently managed firm that has respectable development and margins at a really respectable valuation. In the event that they handle to proceed to develop, not solely EPS might develop however sooner or later in time, right here can also be a very good probability to get a (considerably) larger valuation a number of.

In any case, I began a 4% place at round 42 EUR per share already in December 2024.

As there isn’t a arduous catalyst, the subsequent related date shall be starting of March when Jensen then reviews 2024 numbers. it is going to be particularly attention-grabbing to see if orders have considerably elevated after the TEXCare truthful in November. If enterprise additional accelerates, I would improve the place to a full place.

Annex: Bonus Track: “Soiled Deeds” from ACDC:

https://www.youtube.com/watch?v=whQQpwwvSh4