Again from the Easter break with 20 freshly chosen random Belgian shares. This time, 4 made it onto the preliminary watch checklist.

81. MAATSCHAPPIJ VAN DE BRUGSE ZEEHAVEN (Skilled Market)

At first I bought excited, as this appears to be the Port of Brugge and the port appears to have grown over time in keeping with Wikipedia. And I do like ports.. However this inventory traded final in 2015. Evidently at the next stage, the port has already merged with Antwerpes.

Sadly I didn’t discover any monetary info. “Move”.

82. Mazaro NV

This 4 mn EUR market cap firm appears to be (or have been) an vehicle provider. They IPOed in 2022, however appear to have not reported any figures in 2023. This seems unusual, “go”.

83. CFE

CFE is a 190 mn EUR market cap firm engineering and development firm, majority owned by Belgian HoldCo Ackermans & Van Haaren (62%). French development firm Vinci owns a further 12%.

I got here throughout CFE earlier as CFE was a partial proprietor of DEME (which I personal) however they spinned of the stake within the IPO to their shareholders

The margins have decreased over time, however the inventory may be very very low cost.

Curiously, they had been comparatively optimistic for 2024 of their outlook within the outcomes presentation. I’ll “watch” them as a part of the AvH household.

84. CP76 & CP79 Petrofina (Skilled Market)

There may be additionally a CP 79 PEtrofina on the Skilled market. Each traded final in 2020. They appear to be some form of the rest from former Belgian Oil firm Petrofina, however I didn’t discover out extra. “Move”.

85. Hyloris Pharmaceutical

Hyloris is a 310 mn EUR market cap pharmaceutical firm that has little or no gross sales (3 mn) however important losses. They appear to be public since 2020 and the inventory value now’s roughly on the IPO stage.

I can’t choose in any respect how promising their pipeline is, subsequently I’ll “go”.

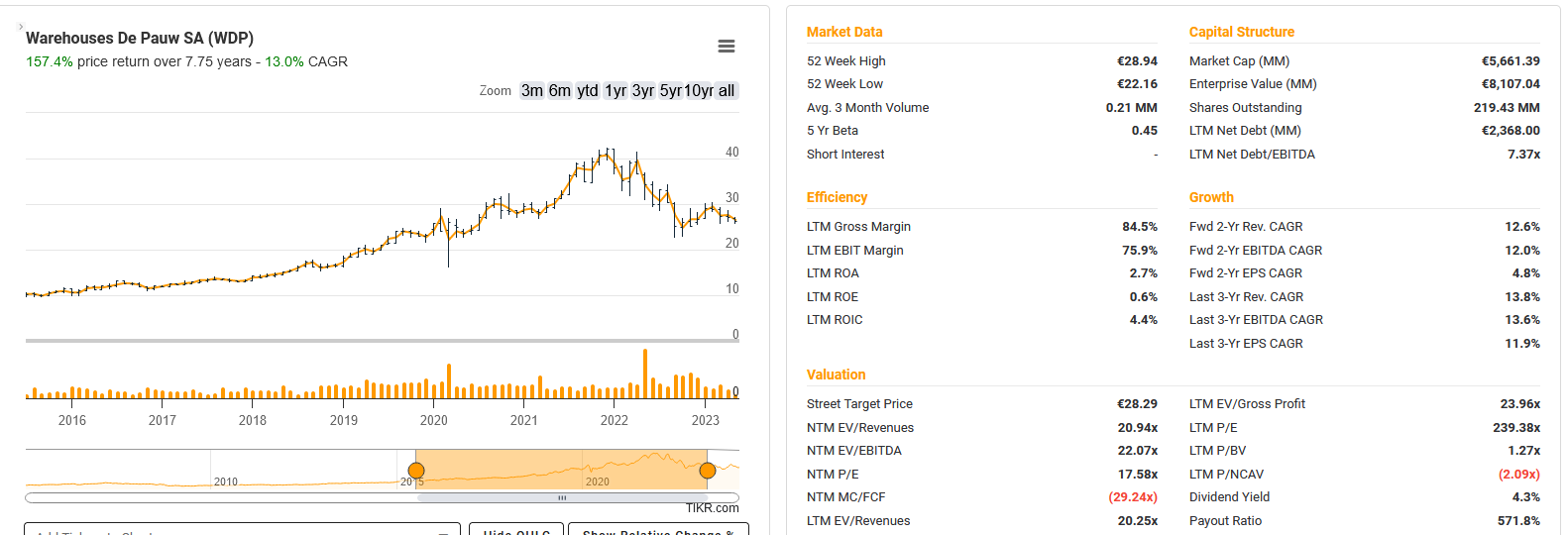

86. WDP (Warehouses de Pauw)

With a market cap of 5,6 bn, WDP is a bigger participant within the logistics actual property house. As this sector nonetheless performs fairly effectively. The De Pauw household remains to be the most important shareholder with a stake of 21%. WDP can be considerably dearer than as an illustration workplace targeted actual property firms, regardless of a pull again within the share value:

Nevertheless, additionally this sector isn’t of curiosity for me, so I’ll fortunately “go”.

87. Ucare Providers

This 0,25 mn EUR Pico-Cap appears to be a house care service that doesn’t launch monetary numbers any extra. “Move”.

88. MICS Companions (Skilled Market)

The Euronext Skilled Market web page doesn’t document any commerce for this one. “Move”.

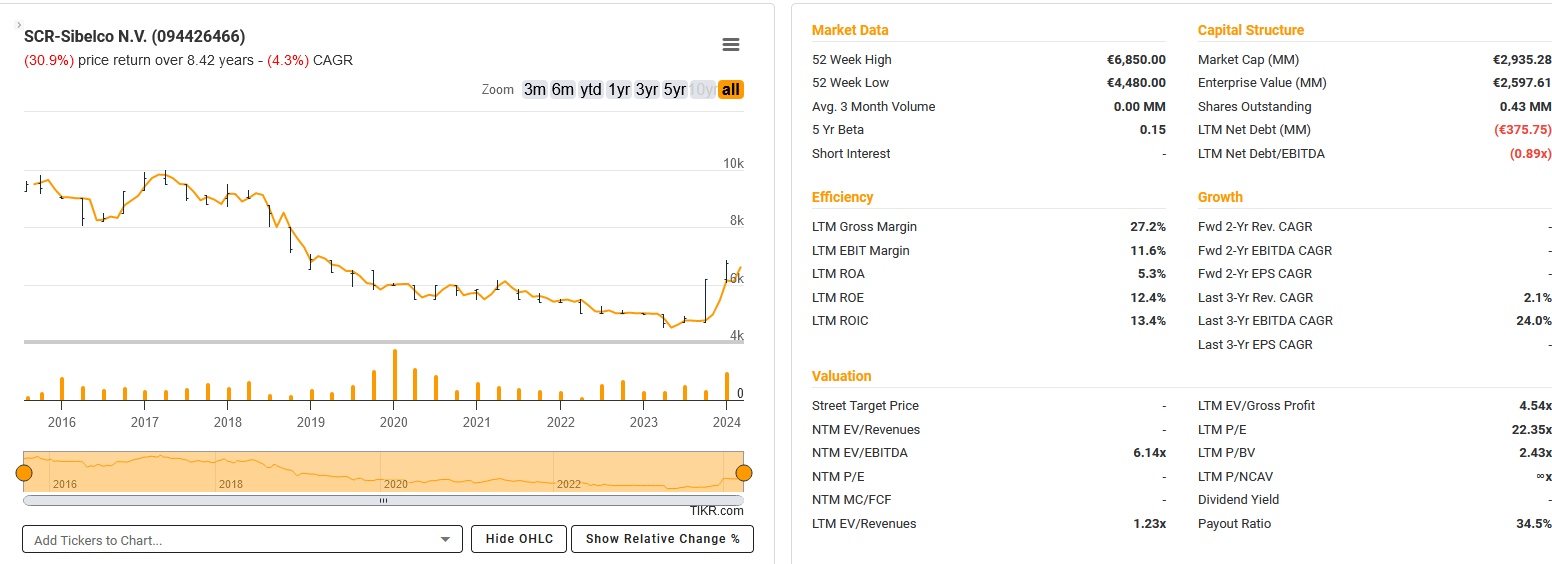

89. SCR-SIBELCO (Skilled MArket)

SCR-SIBELCO is an Skilled Market inventory that trades fairly commonly. Based on TIKR, the have a market cap of two,9 bn EUR which is lots for an OTC inventory:

The corporate is a minerals extraction/mining firm, producing all kinds of supplies used amongst others by PV, Insulation and so on.

that chart from their 2023 report, one can see that the enterprise is sort of risky however 2023 has been a good yr:

Additionally they appeared to have purchased again a major quantity of shares in 2024. It might be actually fascinating to know why such a big firm isn’t listed on the principle change. However anyway, Mining can be not one thing that I do know a number of, subsequently I’ll “go”.

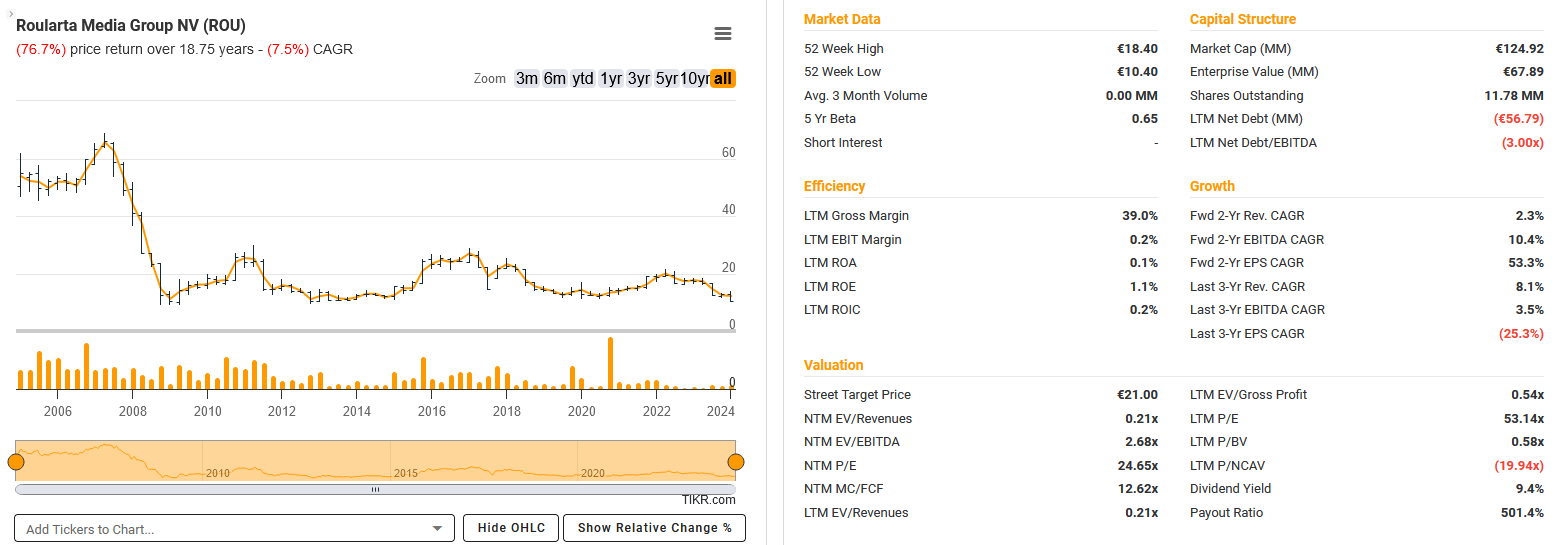

90. Roularta Media Group

This can be a 125 mn EUR market cap Media firm that (sadly) focuses on print magazines and appears to have seen higher days:

The 2023 outcomes give a fairly miserable image:

The corporate sits on some 60 mn of web money, however that appears to deplete fairly shortly, additionally by way of massive dividend funds. Appears an excessive amount of like a melting ice dice, subsequently I’ll “go”.

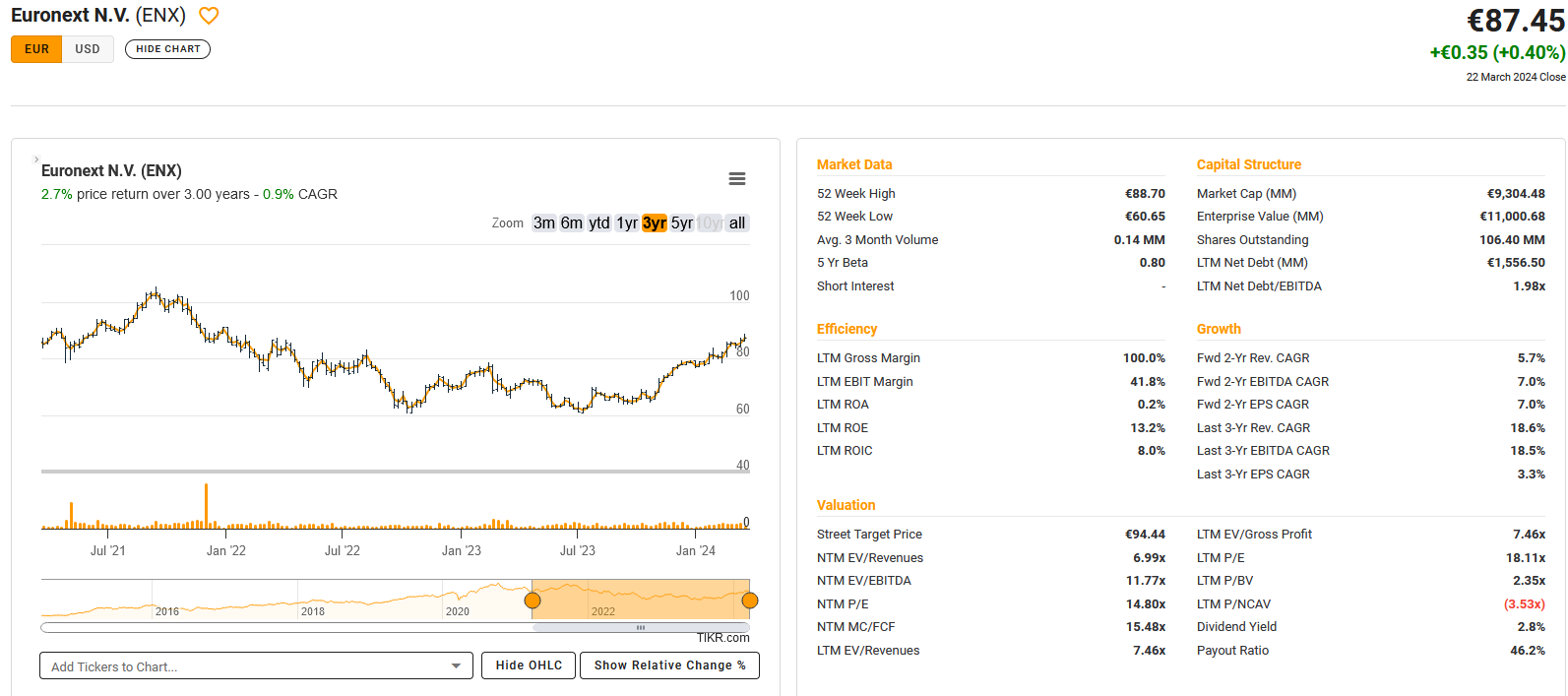

91. Euronext NV

Euronext, with a market cap of 9,3 bn EUR is one other firm that reader of my weblog may know. I purchased a small place in 2021 however excited it in early 2022 with a small revenue as I couldn’t construct up sufficient conviction for a bigger place.

The inventory has been week for a while however has recovered these days to the extent the place I offered it in January 2022:

The enterprise of operating an change is often an excellent one, with the caveat that Europe general has been by some means affected by many take overs, delistings and few IPOs within the latest years.

Euronext enjoys very good margins, 2023 was all in all OK, helped by a great This autumn. For an change operator, the inventory isn’t too costly, though I don’t like all of the changes they’re making in presenting their numbers.

However, that is clearly one inventory to “watch”, particularly if investor curiosity comes again to Europe.

92. BioCartis

BioCartis is a 27 mn EUR market cap Biotech firm that has seen higher days. the corporate is loss making and has important debt. “Move”.

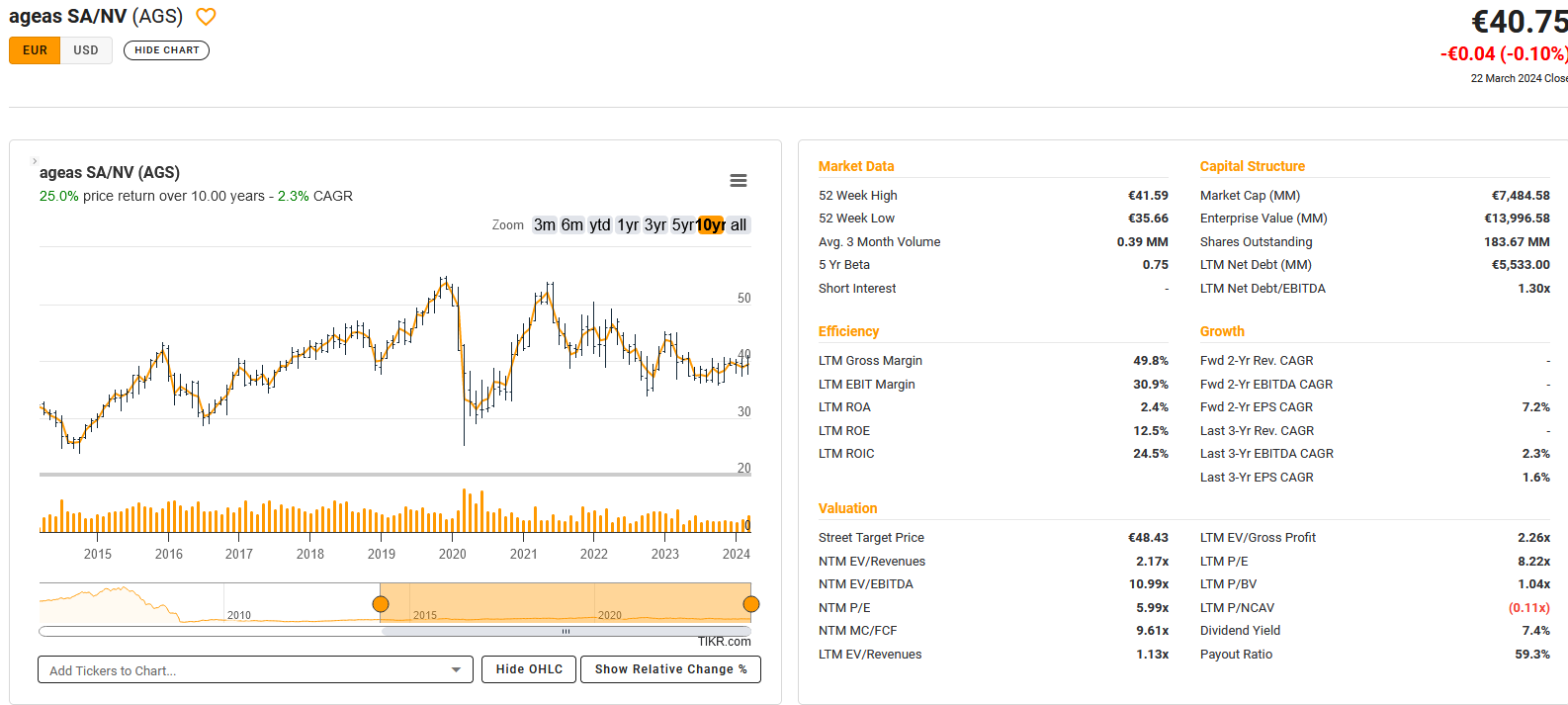

93. Ageas

Ageas, a 7,5 bn market cap inventory, is the insurance coverage arm of former Belgian Monetary Conglomerate Fortis, which went down through the GFC.

Wanting on the share value, we are able to see that nothing huge occurred over the previous 1 years, nevertheless, they pay a really juicy dividend:

The corporate has been shopping for again shares (share depend -10% over 6 years). Very just lately, they made a transfer to accumulate Direct Line within the UK however walked away as Administration of Direct Line opposed the transaction.

Ageas is lively in each, Life and Non-Life enterprise. One very particular side is that round 50% of the operational revenue comes from their Chinese language Life Insurance coverage enterprise.

I believe this additionally explains the low valuation, as traders clearly low cost the earnings from China larger. The biggest shareholder apparently is the Chinese language Fosun Group with ~7%. Ageas itself was all the time rumored to be a take-over goal itself.

I’ll put them on “watch” though I additionally suppose that the excessive share of Chinese language income could possibly be a difficulty.

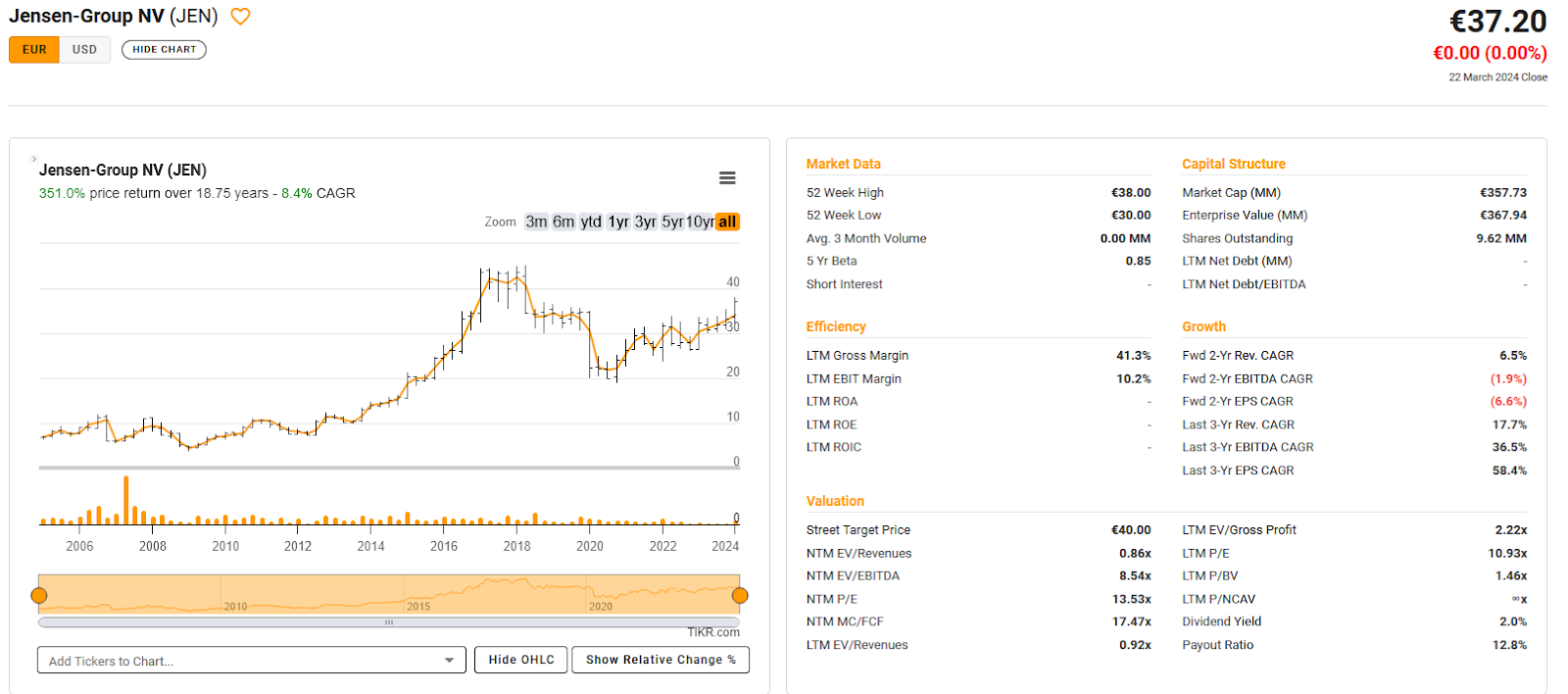

94. Jensen Group

Jensen Group, a 360 mn EUR market cap firm is a specialist for “Heavy obligation laundry” machines, so clearly not your typical family washer.

Apart from Covid, jensen seems like a pleasant “sluggish grower”:

The inventory isn’t too costly and in keeping with TIKR, the household nonetheless owns north of 40%. Curiously, because the identify signifies, the Jensen household is Danish.

2023 was a very good yr for them. Additionally they “swapped” a 20% capital enhance with Property from Miura, a listed Japanese firm, with the intention to enter the Japanese market.

I had appeared on the firm earlier than however I’ve to confess that now I discover them actually fascinating. They may go on “watch” with some precedence.

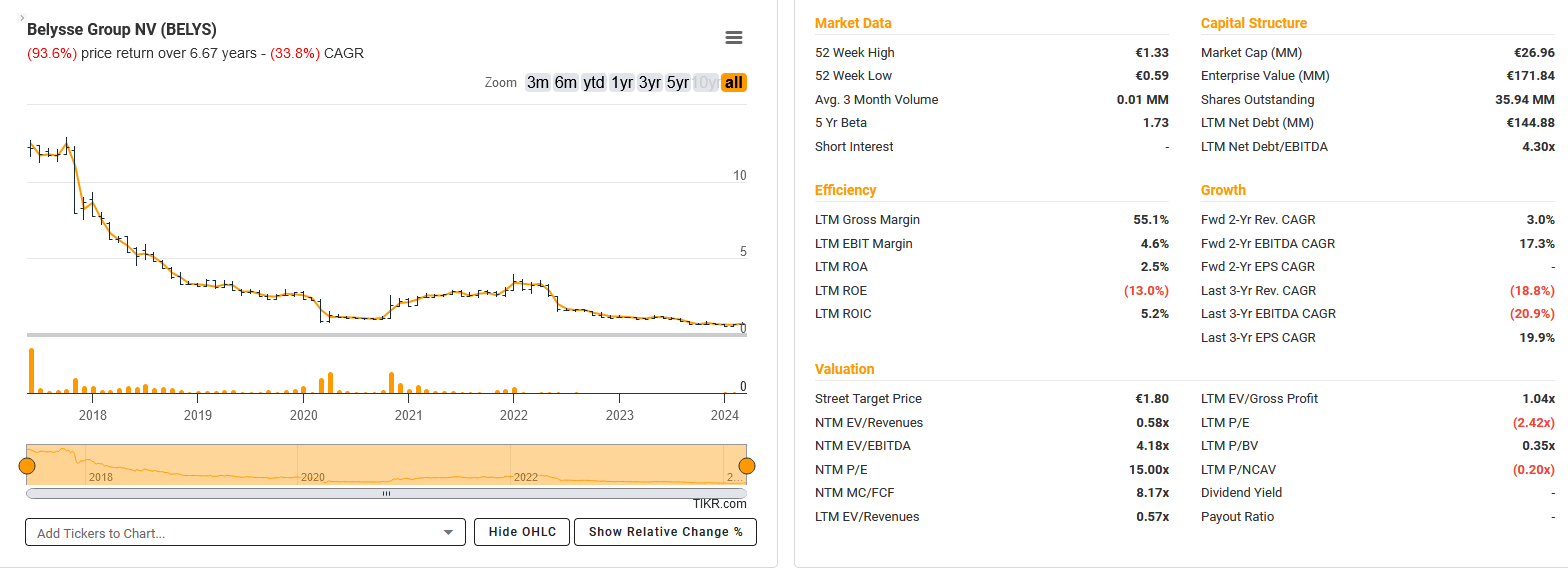

95. Belysse Group

Belysse (previously Balta Group) is a 27 mn EUR market cap firm that manufactures textile flooring overlaying.

Because the inventory chart exhibits, they clearly had higher instances.

Gross sales have halved in Covid and by no means actually recovered, the corporate made losses yearly since then. %4% of the corporate are owned by Lone Star fund, a well-known ”Vulture”. “Move”.

96. Peltzer (Skilled Market)

This Skilled MArket inventory appears to have by no means traded. “Move”.

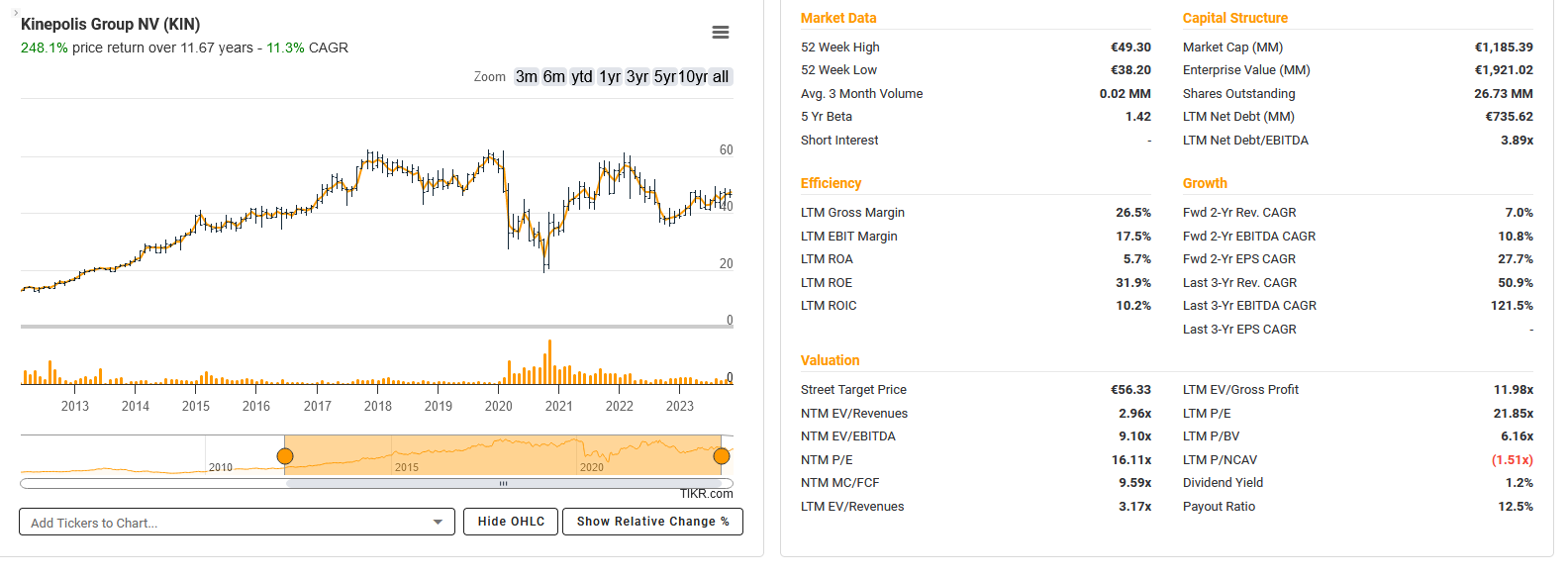

97. Kinepolis

Kinepolis is a 1,2 bn market cap operator and proprietor of film theaters. Wanting on the share value, they held up fairly effectively since Covid regardless of the robust headwinds:

They’re lively in Europe and the US and run the IMAX film theaters. The reporting is sort of good, however I’m not 100% positive how a lot future the film enterprise actually has, particularly because the inventory isn’t actually low cost both. Possibly they may attempt their luck as meme inventory, as their US peer AMC. “Move”.

98. Surongo (Skilled Market)

This inventory traded final in 2018. Googling the identify solely reveals a Bollywood film with the identical title. “Move”.

99. ABO Group

The Belgian ABO Group has nothing to do with the German ABO Wind (which I personal). It’s as a substitute a 60 mn market cap Engineering Group that’s lively in “geotechnics, soil remediation, power, and water and waste administration options in Belgium, the Netherlands, France, and internationally.”.

To a sure extent it’s a small competitor of DEME which presents comparable companies. They managed to double gross sales since 2016, however margins are skinny and the valuation fairly excessive with a P/E of 22x. Free float is small as 86% are held by one individual. “Move”.

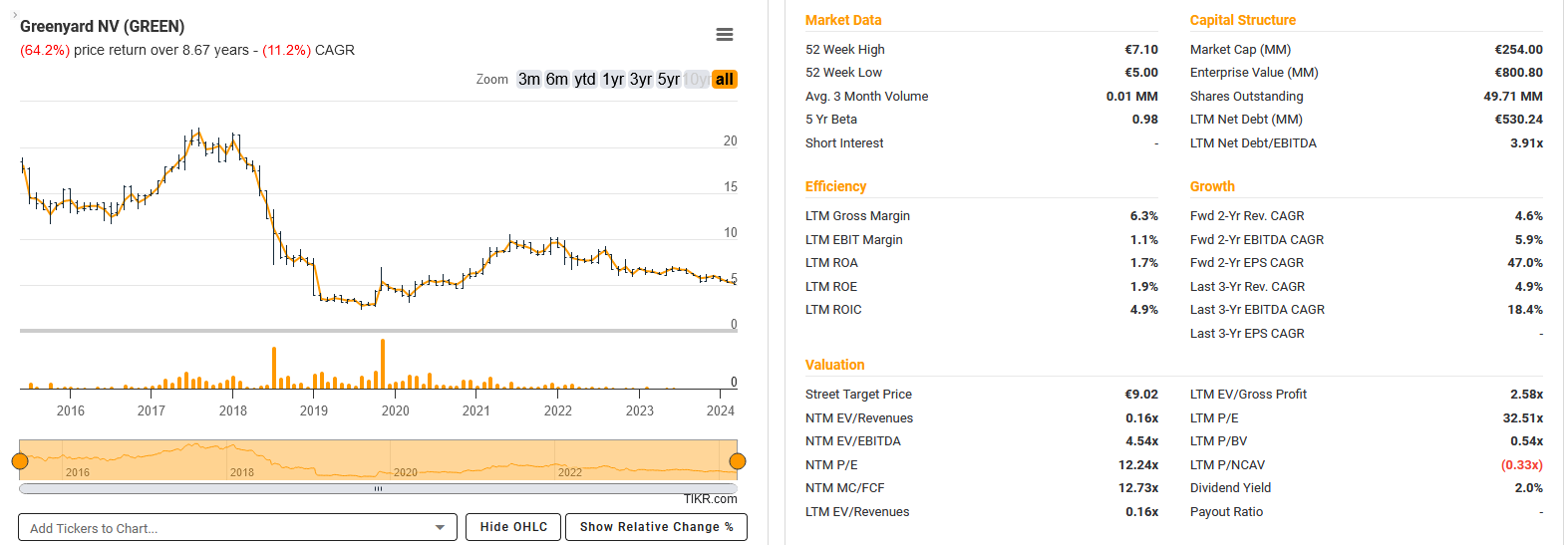

100. Greenyard

Greenyard is a 254 mn EUR market cap distributor of fruit and greens that additionally has seen higher days:

The corporate carries important debt. Margins are skinny and return on capital is low. The investor presentation is filled with changes. Optimistic: The CEO owns 44% of the corporate.

General, it doesn’t look very interesting and the excessive debt is a matter lately, “go”.