Disclaimer: This isn’t funding recommendation. DO YOUR OWN RESEARCH !!!!

As within the earlier write-ups, the total 13 web page doc is hooked up as PDF. Throughout the publish I’ll current the Elevator Pitch, Inventory Value/Valuation, Dangers and Abstract. And naturally a bonus music observe !!

Elevator Pitch:

Amadeus Hearth is a 590 mn EUR market cap small cap enterprise service firm that gives short-term staffing and coaching for finance and IT professionals in Germany. The corporate is effectively managed, has a robust observe document with 10% p.a. progress for a few years, respectable double digit margins, excessive returns on capital and powerful money technology mixed with a transparent capital allocation technique. The present valuation at an EV/EBIT beneath 10x and a fair decrease EV/FCF at appears fairly compelling for such a boring however top quality firm. GARP at it’s greatest in my view.

7. Inventory worth/ Valuation/ Return expectations

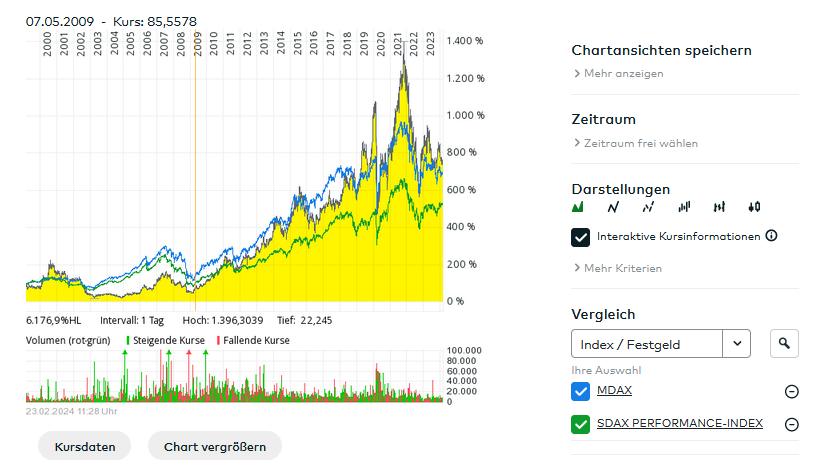

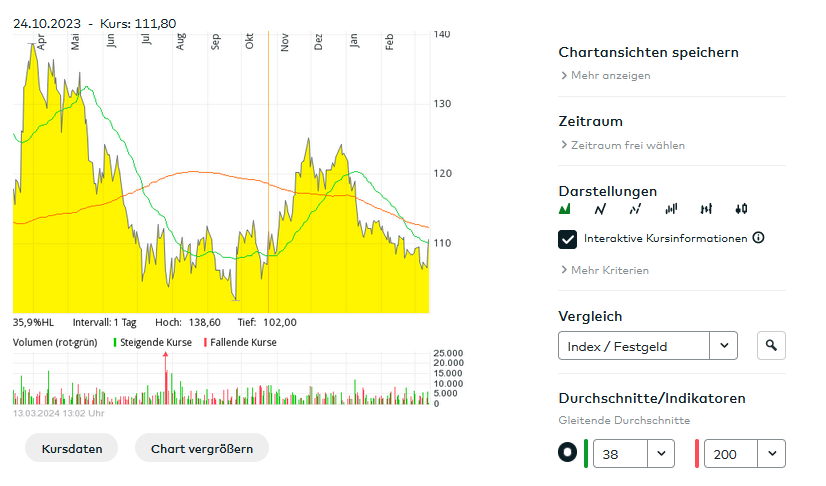

The value chart is kind of attention-grabbing. It took Amadeus Hearth fairly a very long time to surpass the 2001 peak, virtually precisely 10 years till 2011. In any case, the inventory outperformed each, the German MDAX and SDAX even with out together with dividends. The present share worth is roughly the place it was like 5 years in the past, even supposing EPS has elevated by virtually +60%.

Additionally momentum presently remains to be unfavourable:

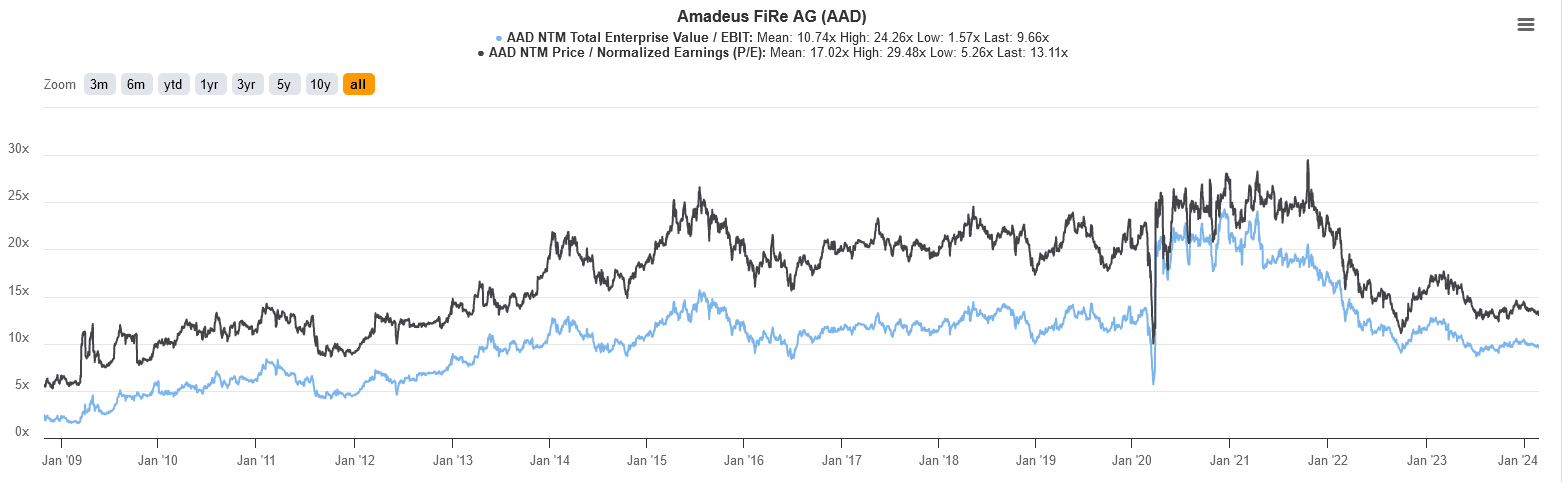

With regard to historic valuations, Amadeus Hearth trades each beneath the long run common for EV/EBIT (9,7 vs. 10,7) and P/E (13,1 vs. 17) which may point out some long run a number of growth potential.

Amadeus Hearth itself final yr confirmed this steerage for future outcomes:

This may roughly suggest whole progress of ⅓ from 2023 to 2026 or ~10 p.a. As talked about earlier than, natural progress requires little or no capital,. I’m not positive hw a lot m&A they want for 10% progress, however I believe a 5% natural progress charge ought to be practical. Even when they don’t handle 10% progress for some purpose or one other, I believe this appears like a really engaging worth proposition, as any a number of extension would come on high.

8. Dangers:

As any funding, additionally Amadeus Hearth clearly faces dangers. Listed here are just a few of them:

8.1. Regulatory modifications

Temp staffing is regulated and rules may change in a option to make it much less engaging. As Amadeus Hearth is barely lively in Germany they’ve full publicity to German regulation

8.2. Dimension of the Area of interest & “Diworsification”

As I attribute Amadeus Hearth’s success to their specialization, any try and “diworsify” outdoors the centered temp staffing (finance, IT) and Coaching would clearly be vital. The query can also be how massive their area of interest is and for the way lengthy they’ll develop in that area of interest by 10% p.a.

8.3. Germany’s financial scenario

The largest threat is clearly that I misread the affect of the present financial scenario in Germany. Low or no progress, structural change, lack of expert staff and inflating wages in my view are all positives for Amadeus Hearth, however after all I may very well be completely fallacious. The identical goes for the growing affect of AI within the office

8.4. Supervisory board member age

As talked about, some members of the Supervisory board are fairly outdated. It must be seen if and the way these members shall be exchanged within the subsequent few years

8.5. Low ball takeover

A closing threat is in my view additionally that with no sturdy shareholder, there is likely to be the danger of a “low ball” take over supply by a competitor or a PE firm. Whereas that may bump up the share worth within the quick time period, it may stop shareholders from collaborating within the full upside potential.

9. Abstract / Sport Plan:

Primarily based on my assumption that the long run for Amadeus Hearth appears not a lot completely different from the previous 5 or 10 years, the inventory provides a possible return of at the least 15% p.a. relying on what natural progress appears like and if they’ll do worth add m&A on high of that.

From a top quality perspective, Amadeus Hearth ticks virtually all containers, with the one exception that there isn’t a founders/giant shareholder current.

For a “top quality” firm, this appears like an excellent worth proposition to me. That’s why I made a decision to allocate an preliminary 3% allocation into Amadeus Hearth at a mean worth of 109 EUR per share.

Amadeus Hearth will launch closing 2023 numbers, their 2024 outlook and the dividend proposal on March nineteenth. Relying if the outlook modifications or not, I would add to the place, particularly if momentum turns a bit bit extra impartial/optimistic.

Additional Bonus Music observe:

As in my final write-up on Eurokai, as soon as once more I add a Youtube Video that expresses my hope for this funding: Rock me Amadeus (Hearth) from Austrian music legend Falco:

Falco – Rock Me Amadeus (Official Video)