Have you ever ever questioned why rich individuals are extra prepared to spend money on hedge funds, enterprise capital, enterprise debt, non-public fairness, and specialty funds? These are all actively-run funds that principally have a historical past of underperforming the S&P 500. But, billions of {dollars} nonetheless pour in annually.

A few of these lively funds are additionally thought of different belongings. Various belongings are typically much less effectively priced than conventional marketable securities, offering a chance to take advantage of market inefficiencies via lively administration. Various belongings embody enterprise capital, leveraged buyouts, oil and fuel, timber, and actual property.

After investing in varied actively-run funds with a portion of my capital since 1999, let me share with you the primary the explanation why I accomplish that by age vary. After a reader requested me for causes in my put up on how I would make investments $1 million, I noticed my causes have modified over time.

Why Folks Make investments In Lively Funds By Age Vary

Our attitudes about cash change over time. Let’s concentrate on them and regulate accordingly.

1) Causes to spend money on lively funds in your 20s: curiosity, naivety, entry

I first invested in a hedge fund referred to as Andor Capital in 1999. The providing was a part of Goldman Sachs’ 401(ok). On the time, Andor Capital had monitor document investing in expertise and I needed in, regardless of the upper charges.

I used to be a first-year monetary analyst with a $40,000 base wage who could not spend money on Andor Capital in any other case. Therefore, I seized the chance. In different phrases, I invested in an lively fund as a result of I had entry. It felt good to be part of a membership – like skipping a protracted line at a preferred evening membership as a result of you recognize the bouncer.

I did not care in regards to the greater charges as a result of I wasn’t investing loads within the first place. In 1999, the utmost contribution to a 401(ok) was $10,000 and $10,500 in 2000. I used to be curious to know what this hedge fund may do.

Andor Capital outperformed throughout the 2000 an 2001 Dotcom bubble bust because it shorted loads of tech shares. In consequence, I walked away with a optimistic impression of hedge funds again then.

Additional, hedge funds have been additionally a few of Wall Road’s largest shoppers. My boss would typically confer with them as “good cash.” If you’re younger, your restricted experiences form your total world outlook. If you wish to get wealthy, it’s higher to be a hedge fund supervisor than to spend money on one.

2) Causes to spend money on lively funds in your 30s: hopes and goals

As you achieve extra wealth a decade plus after faculty, you begin dreaming of what it wish to be actually wealthy. On a yearly foundation, you get bombarded with tales of so-and-so fund supervisor crushing his returns, e.g. John Paulson netting $20 billion shorting mortgage-backed securities in 2008.

You notice that those that get terribly rich in a comparatively brief time period didn’t accomplish that by investing in index funds. Each wealthy investor you hear about obtained wealthy by making concentrated bets. Due to this fact, your pure inclination is to comply with their lead with a few of your capital.

After ten years of lively investing, you’ll lastly begin to notice some vital beneficial properties and losses. For most individuals, their lively investments will underperform the S&P 500 or no matter passive index benchmark. Due to this fact, disillusionment about allocating extra capital to lively funds will creep in over time.

Nevertheless, for individuals who’ve skilled higher wins than losses, the passion for lively investing will proceed. There could be a scenario the place an lively investor earns an enormous proportion return, however a comparatively small absolute l greenback return. In such a state of affairs, the 30-something-year-old you may begin considering, I want I had invested extra!

Your 30s is a time the place you lengthy to earn as a lot cash as attainable. Investing in lively funds or actively investing your cash is constant together with your hopes and goals of someday hitting the massive time.

3) Causes to spend money on an lively fund in your 40s+: safety and capital preservation

After probably twenty years of actively investing, you clearly notice there is a 70%+ probability your lively investments will underperform passive index investments. In consequence, your publicity to lively funds is congruent with actuality.

Try the share of institutional managers underperforming over ten years.

The advantage of investing in lively funds in your 40s is that you need to have extra expertise, wealth, and knowledge. You’ve a greater thought of the place to allocate your non-public capital. You might also have higher entry to traditionally better-performing funds.

In my 40s, I respect a fund supervisor dedicating their occupation to taking care of my capital. The extra skilled the fund supervisor and the higher the monitor document, the extra consolation I really feel. As a result of I have already got sufficient capital to generate a livable passive earnings stream, I optimize extra for peace of thoughts fairly than returns.

When you spend money on an index fund, the fund supervisor has no say within the fund’s investments. As a substitute, the fund supervisor merely buys and sells no matter firm is added or subtracted from the index. However with an actively-run fund, the fund managers have the pliability to guard its traders in the event that they deem it vital.

Given you additionally notice that lively funds can even blow themselves up in any given yr, you make investments accordingly. For instance, few invested in Melvin Capital (-39.3% in 2021, shut down in 2022 after being down 20%+ in 1Q2022) for capital preservation. Slightly, most of its restricted companions invested within the fund in hopes for optimum returns.

Hedging And Diversifying In opposition to Monetary Disaster

Most individuals who get wealthier ultimately go into capital preservation mode. Because the saying goes, “as soon as you have received the sport, there isn’t any must proceed enjoying.” However all of us proceed to play as a result of need for extra. On the very least, we wish to sustain with inflation.

Everyone knows too many tales of people that turned multi-millionaires in a single day and misplaced all of it after which some throughout a crash. For instance, my breakfast sandwich maker remodeled $2 million throughout the 2000 Dotcom bubble. In the present day, he is nonetheless making sandwiches (at a retailer he owns) partially as a result of he did not promote.

Investing in lively funds provides you the potential for higher defending your self towards shedding numerous cash. However one of the best ways to actually shield your self from large losses is to diversify your investments. Investing in lively funds is only one a part of the bigger transfer.

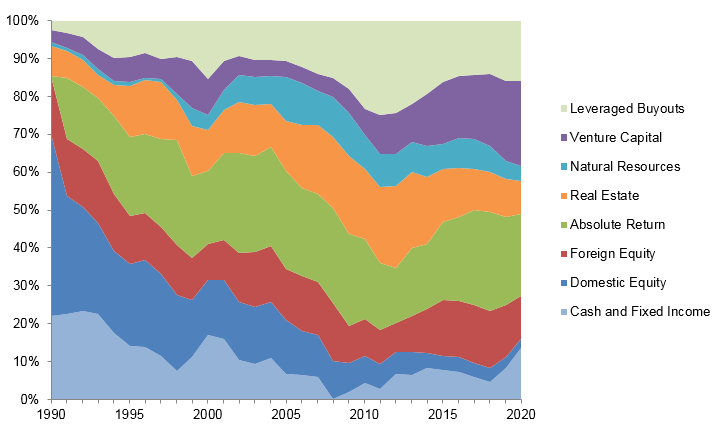

Under is Yale’s endowment asset allocation over time. Discover the small proportion allotted towards home fairness and the big proportion allotted in the direction of varied lively funds.

Let’s Say You Are A Deca-Millionaire

Faux for a second you may have $10 million in investable belongings, the edge the place most consider generational wealth begins. Primarily based on a big Monetary Samurai survey, $10 million can also be the best internet price quantity to have at retirement.

Let’s additionally assume your family spends $300,000 a yr after-tax, which is sufficient to dwell a greatest life. Lastly, let’s assume your family has no lively earnings. The couple determined to barter severance packages and change into ravenous authors as a result of writing is what they like to do.

Primarily based on long-term capital beneficial properties tax charges, incomes a 5% return annually is sufficient to pay for the family’s total annual dwelling bills. Due to this fact, there isn’t any want to take a position the vast majority of the $10 million within the S&P 500, to hopefully earn the historic common return of 10%.

Diversifying For Capital Preservation And Decrease Volatility

As a substitute, the family may minimize up the $10 million into 40% actual property, 30% into public equities, 20% into lively funds, and 10% into risk-free investments.

Actual property is much less unstable and has traditionally paid the family a 7% annual return. The lively funds encompass market-neutral funds and enterprise funds with 10-year vesting durations and historic 6 – 12% returns.

I may simply see this funding asset allocation producing 5% a yr with low volatility. Heck, if there have been no tax penalties, the family must be glad investing $10 million in a one-year Treasury bond yielding 5.2%.

As a result of when you may have $10+ million, the very last thing you need is it to expertise a 19.6% drop in worth, like we noticed within the S&P 500 in 2022. That is a $1.96 million paper loss, or greater than eight occasions the family’s annual bills. The sort of volatility creates anxiousness and stress.

Diversifying your danger publicity by investing in actively-run funds offers each safety and hope. Here is my really helpful break up between lively and passive investing.

I presently have about 25% of my invested capital in lively funds and particular person securities.

Peaceable Residing Is What I Need

One Thursday in Might, I took my three-and-a-half-year-old daughter to the San Francisco Zoo. She solely goes to preschool Monday, Wednesday, Friday, so we spent your entire day collectively.

First we mentioned good day to the giraffes consuming their leaves. Then we visited Norman, her favourite gorilla. On the best way to Little Puffer, the steam practice, we waived good day to Mr. Wolverine.

She had a lot enjoyable waiving to everybody she handed by on the practice whereas the wind made her hair dance. With out a time restrict, we determined to trip the practice once more. I needed to listen to her squeals of pleasure as soon as extra!

As I put my left arm round her shoulder to make sure that she was secure, I felt love and tranquility. At that second in time, I wasn’t targeted on writing or worrying about my investments. All I considered was how fortunate I’m to be right here together with her on a weekday afternoon.

The sentiments of peace, love, and tranquility are priceless. They dwarf the sensation of constructing a better charge of return on some funding. Given these emotions are priceless, I do not thoughts paying lively administration charges to individuals I belief who may higher shield my cash.

I am underneath no phantasm that my lively investments or lively funds will outperform the S&P 500 index a majority of the time. However I do know that every time there’s a large drawdown within the S&P 500, it would really feel nice if I do not lose as a lot cash.

As you get wealthier, you might also be extra prepared to pay for higher peace of thoughts as properly.

Reader Questions And Strategies

In case you are an lively investor, have your causes for actively investing modified as you have gotten older? Have your views on investing in index funds modified as you have gotten wealthier?

Enroll with Empower, the very best free device that will help you change into a greater investor. With Empower, you’ll be able to monitor your investments, see your asset allocation, x-ray your portfolios for extreme charges, and extra. Staying on prime of your investments throughout occasions of uncertainty is a should.

Choose up a replica of Purchase This, Not That, my prompt Wall Road Journal bestseller. The e book helps you make extra optimum funding choices so you’ll be able to dwell a greater, extra fulfilling life.

Be part of 60,000+ others and join the free Monetary Samurai e-newsletter and posts through e-mail. Monetary Samurai is likely one of the largest independently-owned private finance websites that began in 2009.

{kind=link}