We’re at the moment in a market the place one week appears to be already an extended time period. One week in the past I wrote about Silicon Valley Financial institution and the completely different cycles in a typical banking disaster (First liquidity, then credit score troubles).

Final week: SVB

In between, the financial institution run accellerated and SVB was then closed and rescued by the FDIC. Within the age of social media, there may be now a variety of protection on this occasion accessible, personally I discovered this Odd Tons Podcast Episode useful in addition to Matt Levin’s take. Matt Levin additionally has a solution on why SVB was not offered over the weekend: Within the wake of the GFC, most of the banks who purchased failing lenders have been then punished with lawsuits and evidently one thing like this might occur to SVB as effectively.

Present consensus is that SVB failed each, due to very unwise rate of interest bets on its asset aspect in addition to an unhealthy focus of its depositor base related by a couple of large VCs on its legal responsibility aspect. In response to many tales, SVB was a really lively member of the Silicon Valley VC ecosystem and one way or the other the VCs (and startups) mainly killed the Goose who laid them golden eggs with this bankrun. Within the present tough funding setting, It will have made extra sense fot the VCs to assist the financial institution however I assume they have been all in panic mode.

This week: Credit score Suisse

This week, the remark of a consultant of the Saudi Funding fund led to the implosion of the share worth of Credit score Suisse. Someday later, the SNB and FINMA launched a press release that they’ll backstop 50 bn of liquidity necessities which for now appears to have stabilized issues to a sure extent.

Credit score Suisse – Rogue Financial institution

CS was a gradual shifting prepare wreck ever for the reason that former McKinsey “Wunderkind” Tidjane Tiam took over as CEO in 2015. When he was fired in 2020, not solely it was revealed thaty he used personal investigators to spy on fellow board members, however extra importantly, Credit score Suisse was concerned in nearly each main fuck-up in the previous couple of years. A number of examples:

- 5,5 bn USD loss with Archegos/Invoice Kwan in 2021

- 1,7 bn USD loss with Greensill

- Pushed 1 bn of Wirecard bonds into Purchasers portfolios shortly earlier than the collapse

- Was a creditor to Chinese language faux espresso chain Luckin Espresso

- CS is meant to carry not less than 80 bn USD belongings of criminals and corrpupt politions

Solely up to now few months, the Swiss regulator overtly critisized CS’s weak controls and in addtion, CS discovered “materials weaknesses” of their monetary reporting. For extra unhealthy stuff, simply googling “Credit score Suisse scandal” provides extra outcomes on cash laundering, Bulgarian Cocaine rings and different “juicy” stuff, it’s actually unbelievable.

Wanting on the CS share worth, it’s fairly apparent that there’s actually no backside:

Though it’s all the time very tough to make predictions, I personally assume {that a} true and lasting turn-around for CS could be very unlikely. There are only a few instances in banking historical past the place a monetary establishment survived such a “clusterfuck”. Credit score Suisse wouldn’t be the primary large title in Banking that simply disappears. In addition to Leahman and Bear Stearns, who remembers Salomon Brothers, DLJ, Bankers Belief, Barings, Smith Barney, Chemical Financial institution, Dresdner Financial institution and all of the others ?

The more than likely state of affairs for my part will likely be that the ring-fenced Swiss operation will one way or the other survive. What meaning for Bondholders and shareholders on Group degree is open, however for my part the CS shares are at greatest a “far out of the cash possibility” on a really optimistic state of affairs. After all something could be traded profitably within the quick time period, however mid- to longterm, a whole lack of capital could be very seemingly for CS shareholders.

At this time: First Republic Financial institution

First Republic, a “mid sized” 200 bn plus US financial institution with ~21 that banks to “Excessive web price shoppers in costal areas” continued its plunge and stated it could be open to nearly something, together with a hearth sale with the intention to survive.

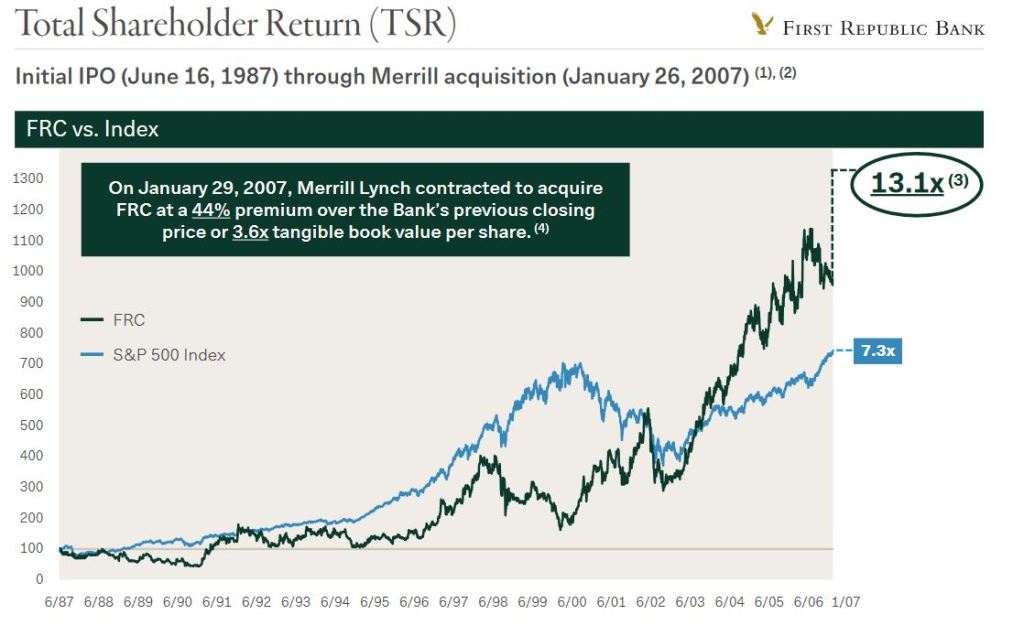

When studying the January invetsor presentation, First Republic appears to be like like an absolute success story, amongst others, their share worth went up 13x since 1987, nearly 2x the extent of the S&P (i assume ex dividends) which is outstanding for a financial institution:

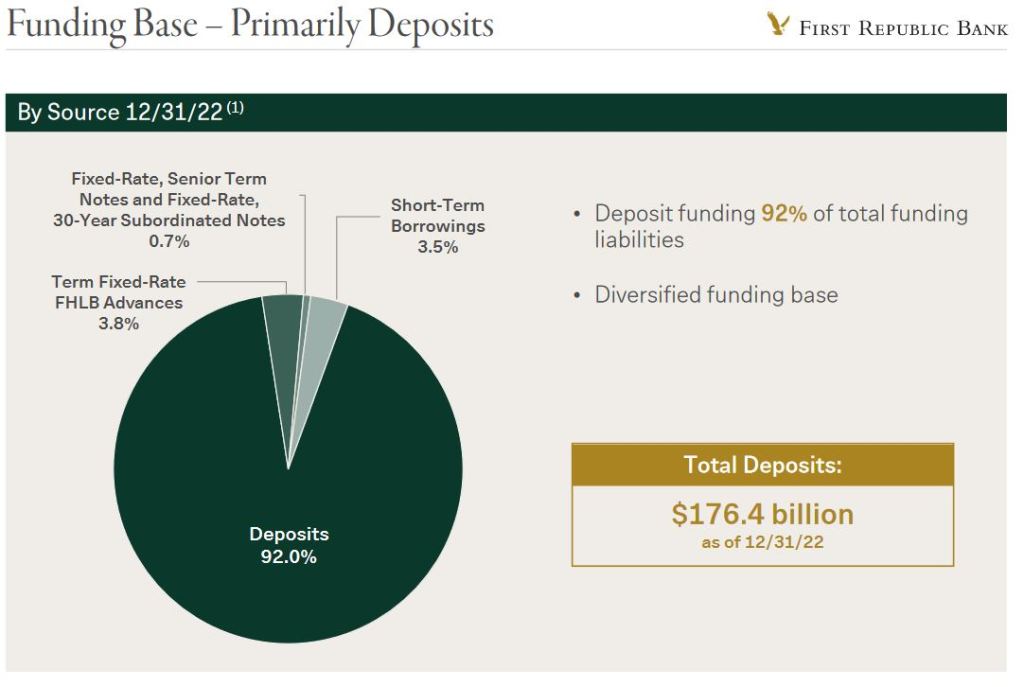

Nonetheless, these slides, it turns into comparatively clear the place the issues of Republic are: Funding is generally by way of deposits:

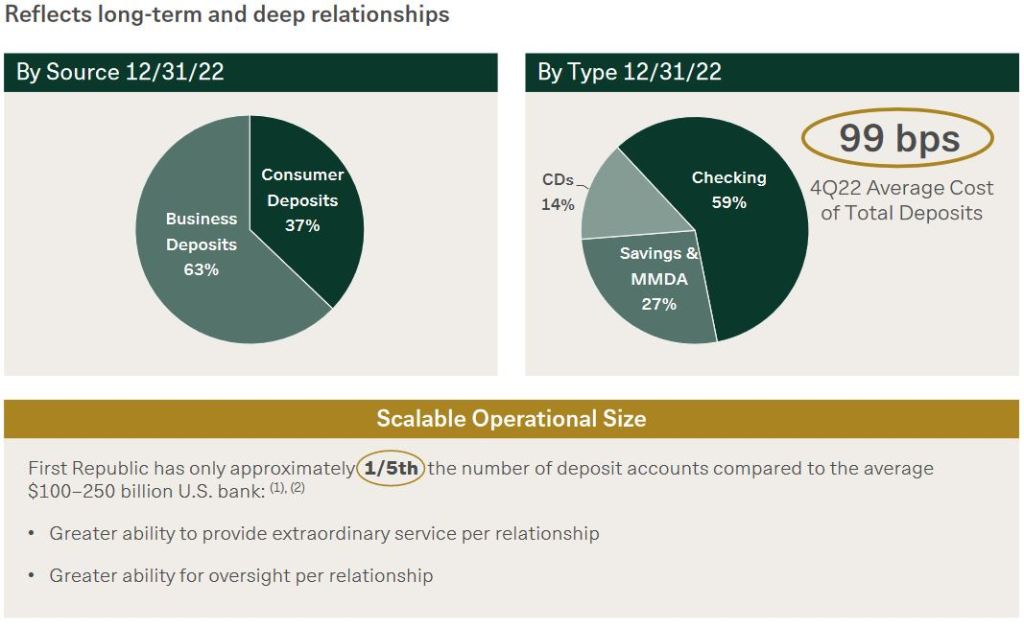

The deposits are principally enterprise accounts and bigger dimension:

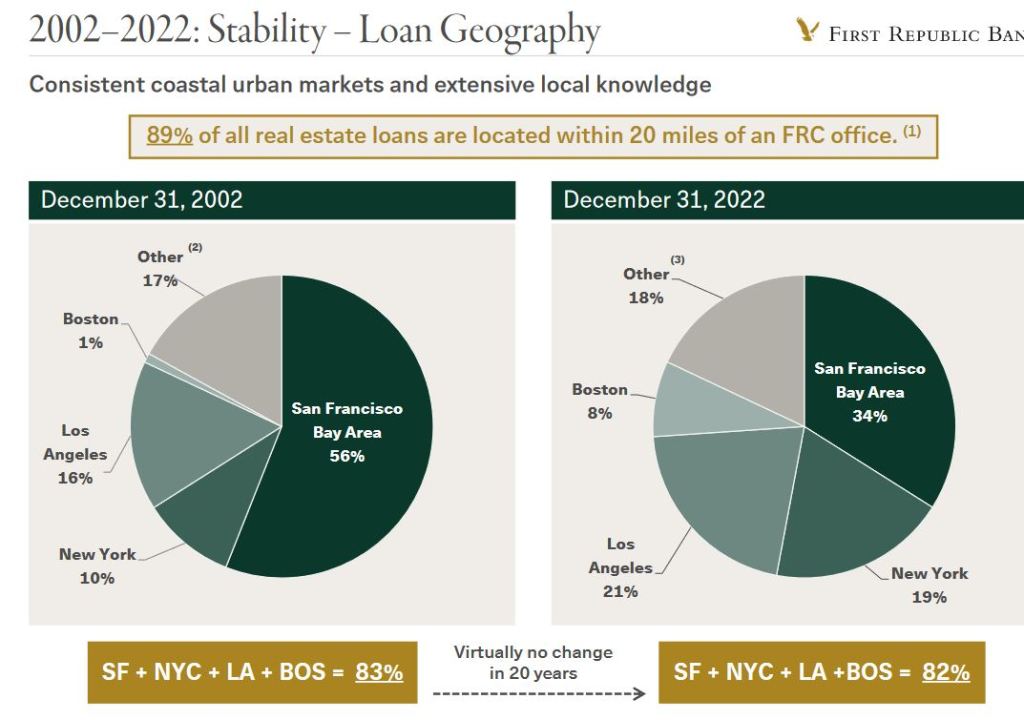

And, the Asset aspect consists principally of “coastal actual property loans” and enterprise loans to venturec Capital funds, each belongings that could be in hassle:

It didn’t assist that the Ranking Companies simply downgraded First Republic to “junk” due to the weak funding construction.

To be sincere, If I’d have identified about First Republic earlier and skim the investor presentation, I might need thought-about it as a possible funding. The financial institution additionally traded at uncommon excessive P/E multiples within the vary of 20-30 earnings, so only a few traders

Subsequent week and thereafter: What may very well be the extra lasting results of this episode ?

I assume that for the following two or extra weeks, the market is “looking” for additional weak gamers and all of them will likely be backstopped by their respective Governments and Central Banks. A “Lehman second” for my part nonetheless stays a really low likelihood state of affairs. Nonetheless it is usually clear that this complete growth might need wider penalties.

For the banks, it will likely be much more tough to remodel quick time period deposits into long term belongings, which by definition is without doubt one of the major perform of the banking system. For the US, extra and more durable regulation is already on the way in which.

Amongst different unwanted side effects, total the present growth will more than likely improve funding value and restrict borrowing capability for the banking sector. This in flip will make it tougher for debtors to acquire or roll over financial institution loans. And if debtors are capable of get hold of financial institution loans, they might want to pay larger credit score spreads. A sure improve in Company Credit score spreads was already observable up to now few days.

General this might have a siginficant affect on enterprise exercise as the supply of financial institution loans is a number one indicator for financial exercise. This in flip may then result in the second a part of the cycle, the actual credit score cycle with extra defaults and so on.

Relying on how inflation charges are growing, the central banks may counter with decrease rates of interest, which nonetheless, do little to make lending simpler for the banks. After all, Governements and Central banks will attempt to counter an enormous credit score squeeze, nonetheless with out tighter credit score situations it’s unlikely that inflation will cool off rapidly.

I want to emphasise right here that I’m not a Macro man in any respect, however total, I believe the likelihood for an actual credit score cycle has elevated considerably. As a consequence, for my part one ought to restrict publicity to uncovered monetary corporations in addition to companies with close to or mid time period funding necessities.

{kind=link}