As tens of millions of child boomers method retirement with Era X-ers not far behind the query of “Are you able to retire with $500,000?” repeatedly pops up amongst our readers. But, it’s not solely these 60-year-olds enthusiastic about retirement, but additionally, we discover middle-aged of us asking if retiring at 55 with 500k is cheap.

This text will delve into these questions:

- Can I retire with $500,000?

- How a lot do I must retire at 60?

- How lengthy will $500,000 final in retirement?

- Tips on how to retire ceaselessly on a set chunk of cash?

- When must you retire?

As if it’s not sufficient for these older adults questioning, “Can I retire at 60 with 500k?” many people of their 30’s and 40’s at the moment are striving for early retirement and monetary freedom. This new era of younger and center aged adults in search of early retirement have even shaped their very own neighborhood, FIRE – Monetary Independence Retire Early.

So, for those who’re desirous about the best way to retire ceaselessly on a set chunk of cash, or methods to retire on 500k, you’re in the proper place! In reality, you simply may discover out that it’s attainable to retire at 45 with $500,000.

Are you able to Retire on $500,000?

Like every monetary query, “Can I retire on 500k?” relies upon upon many elements:

- What retirement means to you

- How a lot cash you want annually

- Your anticipated life-style in retirement

- Your geographic location

- Your present investments

- Different sources of revenue

- Whether or not you need to work part-time in retirement or not

The best response to “Are you able to retire on 500k?”, is to determine two issues:

- What is going to your retirement life-style will value?

- How a lot revenue may a $500,000 funding portfolio generate. In different phrases, for those who make investments $500,000 will the returns from that portfolio assist your life-style?

How a lot cash do you should stay on?

To start out our evaluation, we’ll make some assumptions. You may modify them, to suit your private scenario. Later within the article, you’ll study methods to tweak your retirement value of dwelling.

Let’s assume that you simply’ll want $49,000 per family per yr to stay on, the bureau of labor statistics common for retirees.

This quantity could also be larger or decrease relying upon the place you reside and your life-style in addition to your projected well being care bills.

To personalize this evaluation, take a couple of minutes to map out how a lot you count on to spend in retirement. Contemplate spending for fundamental dwelling prices and extras reminiscent of journey and presents. Assess how your put up retirement spending will change.

Associated: Tips on how to Save For Retirement at 30 and Turn out to be a Millionaire

Take into consideration whether or not your imaginative and prescient of retirement consists of any cash making actions, facet hustles or half time jobs.

After you have your estimated funds, you’ll be able to start to find out whether or not it’s attainable so that you can retire at age 60 with $500,000.

Top-of-the-line retirement planners is FREE from Private Capital. I exploit it and the arrange is quick and safe. Click on under to attempt the retirement calculator and instruments.

Tips on how to Retire on 500k with a Variable Withdrawal Fee to Preserve a Regular Revenue Degree

As a substitute of adhering to a traditional withdrawal fee, just like the 4% rule, our preliminary evaluation makes use of your anticipated funds in retirement to reply the query, “Can I retire at 60 with 500k?”

As with all future planning, particularly the best way to retire ceaselessly with a set chunk of cash, you’ll must make some assumptions.

Retire on $500K Funding Assumptions:

Spend money on a diversified mixture of 60% inventory investments and 40% bond funds,

Use their historic returns together with changes incorporating the present financial state of affairs.

Earn an anticipated common annual return of 6.4%.

Conservatively, we mission 8% returns on the inventory funds and 4% returns on the bond investments. Be cautious of aggressive return projections.

In fact, you may assume a special asset allocation and enter different funding returns, relying upon your private scenario and evaluation of future returns. However we suggest conservative assumptions when analyzing whether or not you’ll be able to retire on 500k.

Tips on how to Retire at 60 With 500k – Assumptions:

- Your present age is 60 years outdated.

- Life expectation is 90 years outdated.

- Your 60% inventory 40% bond portfolio will earn roughly 6.4% yearly

- Your annual dwelling bills are $49,000

- Inflation expectation 1.5%

- Declare Social Safety at age 62

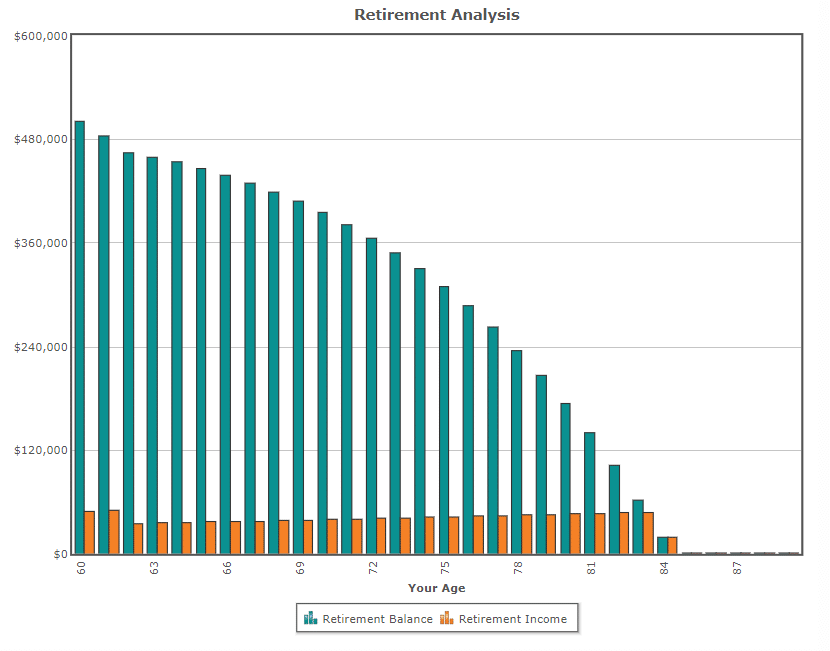

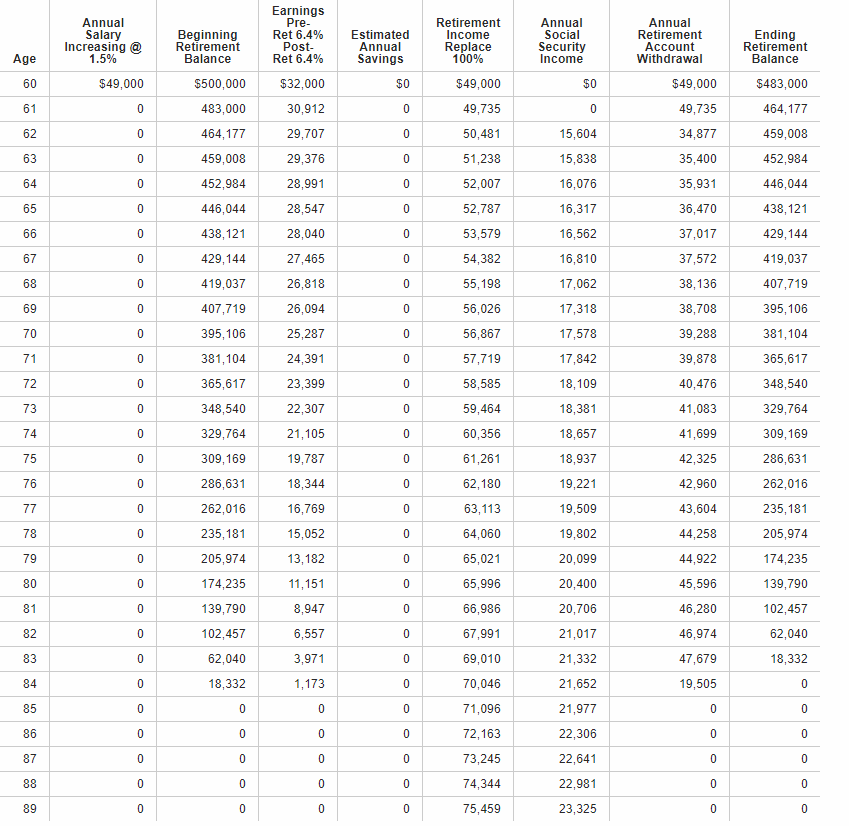

We used a retirement calculator to provide you with the next information:

Retirement Revenue Projections for a 60 12 months Outdated With $500,00

Calculator supply: https://www.calcxml.com/calculators/retirement-calculator?skn=#detailedResultsTop

With the assumptions above, your $500,000 account shall be depleted by age 85. After that point, your revenue will consist solely of Social Safety.

Right here’s how the numbers work out:

However, don’t despair, we will nonetheless flip the query of “Can I Retire at 60 with 500K?” right into a sure, with just some minor changes!

First take into account the assumptions.

Your Social Safety Funds could be larger than the assumtions. Moreover, you might need a working partner or a facet hustle that generates money move. Your private scenario will affect the response as to if you’ll be able to retire at 60 with $500k.

Let’s check out the best way to retire ceaselessly on a on a set chunk of cash. It’s not straightforward, however it’s do-able.

Tips on how to Retire on $500K?

Let’s tweak our assumptions a bit and determine the best way to retire with $500k at age 60. In any case, complement your revenue or modify your life-style and the numbers can work in your favor.

1. Wait to assert Social Safety

By ready to assert Social Safety, you improve your advantages by roughly 8% per yr. So, the longer you’ll be able to wait to assert your advantages, the much less cash you’ll must fund your retirement.

Meaning you’ll must slash bills and earn a bit throughout your first years of retirement, with a purpose to complement the dearth of Social Safety throughout your first 5 years of retirement.

In the event you’re actually fortunate, you might need a working associate to complement the retirement invoice till Social Safety kicks in.

2. Slash your dwelling bills for the primary few years in retirement.

Reducing bills is without doubt one of the best methods to make your retirement {dollars} go additional.

There are numerous methods to slash dwelling bills in retirement. You may downsize your house and your automobile. Cut back discretionary bills reminiscent of costly journey and eating out. Keep away from supporting grownup kids, who must be on their very own.

The Bureau of Labor Statistics discovered that older American households spent a median of $45,700 per household. So, if we’re contemplating whether or not a single grownup can retire at 60 with $500K and never a pair, it shouldn’t be too troublesome to chop again on retirement bills.

In the event you reduce bills by $4,000 per yr or $11 per day, the numbers work to retire at age 60 with $500,000.

“In the event you select to stay on $45,000 per yr, you may declare Social Safety at age 62 and absolutely fund your retirement till age 90.”

3. To Retire with $500k, take into account transferring to a decrease value of dwelling space.

Top-of-the-line methods to slash retirement bills is to maneuver to a decrease value of dwelling space. Taxes, housing and meals prices range considerably throughout the nation, and the globe!

Though I presently stay within the San Francisco bay space, the most costly area within the nation, I’ve lived in Indianapolis, Central Pennsylvania, and Southern Ohio, all considerably extra inexpensive places. Truly, dwelling in decrease value of dwelling areas gave me and my household the chance to aggressively develop our investments and finally have the ability to stay in California.

By slashing housing, meals and tax bills, you’ll be able to reduce out tens of 1000’s of {dollars} out of your annual funds.

In keeping with a current Pockets Hub research, the bottom value of dwelling areas for retirement within the US embrace:

- St. Petersburg, Florida (tie)

- San Antonio, Texas

- Knoxville, Tennessee

- Birmingham, Alabama

- Tallahassee, Florida

- Cellular, Alabama

- Jacksonville, Florida

You could be stunned which you can stay close to the seashore on a funds as effectively. The HGTV present, Beachfront Cut price Hunt follows households throughout the nation shopping for inexpensive houses on the water.

For the adventurous, expatriate communities throughout the globe facilitate retirement in stunning worldwide places, for a fraction of the price of dwelling within the US.

4. Discover a Retirement Aspect Hustle

“Amongst 65- to 74-year-olds, labor pressure participation is predicted to hit 32 % by 2022, up from 20 % in 2002.” ~ AARP.org

With lifespans rising, many older adults want to not retire of their 60’s within the conventional sense, solely to face 30 years out of the workforce.

Even for those who’re hesitant to work part-time throughout retirement, aside from the money move, there are important advantages to working in retirement:

- Ready to assert Social Safety will probably present higher lifetime advantages.

- You may obtain medical health insurance.

- Working in retirement retains your thoughts engaged and may promote higher well being and well-being. In reality, a College of Oregon research that it’d even add years to your life.

- A second profession or facet hustle may improve your life satisfaction.

Can I Retire But?

The reply to the query, “Can I retire but?” is decided by a number of main elements:

- How a lot you spend in retirement.

- The dimensions and composition of your funding portfolio.

- What returns you’ll obtain out of your investments.

- While you declare and the quantity of Social Safety advantages you’ll obtain.

- How a lot further revenue you’ll be able to count on.

The difficult half is that almost all of those questions have versatile solutions. So, it’s your job to make your greatest estimates.

For a 60 yr outdated, retiring with $500,000 is achievable. By investing properly, spending sensibly, and selecting to stay in a fairly priced location $500,000 can assist a life-style of spending roughly $45,000 per yr.

But, there are a lot of youthful of us trying to retire early and questioning if retiring at 55 with $500k is feasible.

As a bonus, let’s have a look at different retire-early situations and discover, “What’s an affordable sum of money to retire with?”

Tips on how to Retire Ceaselessly on a Mounted Chunk of Cash – Bonus Part

To retire ceaselessly on a set chunk of cash, you’ll must handle your saving, investing, life-style, and take into account a facet hustle.

Mr. Cash Mustache did a pleasant evaluation for this query with a number of situations. All his analyses included spending $40,000 per yr in retirement and having both; $800,000, $1 million or $1.3 million in investments.

That’s some huge cash, for a lot of of us to accrue earlier than they hit age 60. But, it’s attainable to construct up a hefty portfolio comparatively rapidly with aggressive saving, investing, and easy dwelling.

To retire ceaselessly on a set chunk of cash, you’ll must construct up a 6 to 7 determine funding portfolio or stay in a foreign country.

You may construct up a $1,000,000 funding portfolio in 25 years by investing $14,776 per yr in an funding account incomes 7% per yr. Keep away from placing all the cash right into a tax deferred account like a 40(ok) and IRA as a result of you’ll be able to’t withdraw that cash penalty free till age 59 ½. So, it’s clever to speculate outdoors the retirement account as effectively in a brokerage account at one of many low cost corporations like Schwab, TD Ameritrade, E*TRADE, or Vanguard.

To develop your investments to $800,000 in 25 years, you’ll want to speculate roughly $11,820 per yr.

Whereas saving $14,776 or $11,820 per yr looks as if some huge cash, understand that any moneys diverted right into a 401(ok) reduces your taxable revenue.

To construct up your monetary portfolio for the longer term, an alternative choice is to develop your revenue, so as to save and make investments much more aggressively.

The opposite issue to retiring ceaselessly on a set chunk of cash resides merely. You want a dedication to chop bills and stay on a funds. Or, earn a big revenue.

Associated: Tips on how to Earn Cash On-line for Seniors

Many early retirees want to do “work” that they take pleasure in and complement their financial savings. In the event you fall into that camp, then it’s a lot simpler to “retire early” for those who’re additionally bringing in some revenue.

Finally, build up a bit of cash to fund your life is a numbers recreation. Reside affordably, save and make investments aggressively to retire ceaselessly on a set chunk of cash.

The 4% Rule – How Viable is it?

Put forth by William Bengen in 1994 after learning 50 years of historic funding market returns the 4% rule states that most often, for those who withdraw 4% of the worth of your funding portfolio annually, your cash ought to final for about 30 years.

Properly, dwelling for 30 years after retirement is nice for those who’re 60, however for those who’re 50, and you reside till age 90, then the final 10 years with none financial savings, gained’t be too nice.

So, if we tweak the rule a bit and withdraw 3% of your investments let’s see how a lot cash you’d want to succeed in $40,000 per yr.

In the event you withdraw 3% from a $1.35 million portfolio, you’ll have an annual money move of $40,500 per yr and it’s unlikely that the portfolio would ever be depleted.

Learn: Which Accounts to Faucet First in Retirement

However wait, listed here are some methods to scale back the required retirement lump sum or construct up money extra rapidly:

Make investments extra aggressively and mission a better fee of return. In the event you allotted a higher % of your investments to inventory market investments, you will have the opportunity of incomes larger returns. With an 8.5% annual common return, you’ll be able to construct up a $1,000,000 portfolio in 20 years by investing $19,000 per yr.

Earn simply $20,000 per yr, and also you’ll want far much less to retire early. So, working part-time, particularly in a facet hustle that you simply take pleasure in, could make early retirement a lot simpler.

In reality, most FIRE of us aren’t trying to retire early and do nothing. Lots of them need to depart their present jobs to work in a means that appeals to them.

When Ought to You Retire?

Because the examples and dialogue illustrate, there are an abundance of things that go into the questions of whether or not you’ll be able to retire with $500,000 in financial savings or how a lot you should retire. Not the least of which is, “What does retirement imply to you?”

Truly, for those who hate your job, possibly all you want is a job you want extra. Or, for those who’re nearing age 50, really feel such as you’ve put in your hours and have constructed up a good portfolio, then retiring at 55 with $500k is certainly attainable.

As with every life selection, there are at all times tradeoffs, and only a few individuals and have all of it. If retirement means dwelling solely off of your investments and Social Safety advantages then you definitely’ll want a a lot bigger portfolio than for those who’re in search of a easy life on the coast of Texas when you work part-time on the Residence Depot. Or possibly a low-fee Annuity would assist stabilize your retirement revenue.

No matter your future holds, there are a lot of on-line calculators that will help you map out your retirement future.

Advisable Retirement Calculators:

Private Capital Retirement Planner – Complete Free On-line Retirement Calculator. After a fast join, simply navigate to the Retirement-planner web page.

OnTrajectory Retirement Calculator – Free On-line Retirement Caclulator with Paid Improve

Vanguard Retirement Calculator – Free On-line Retirement Caclulator

CalcXML – Free On-line Retirement Caclulator

MaxFi Planner – A fee-based retirement and monetary planning instrument.

Disclosure: Please notice that this text might comprise affiliate hyperlinks which signifies that – at zero value to you – I would earn a fee for those who join or purchase by the affiliate hyperlink. That stated, I by no means suggest something I don’t imagine is effective.

Featured picture credit score: Photograph by Khachik Simonian on Unsplash

{kind=link}