Lot’s of ships this time plus a bit of fish. General, these 15 randomly chosen Norwegian shares resulted in 4 candidates for my preliminary watch listing. Let’s go:

76. Klaveness Mixture Carriers

Klaveness is a ship proprietor that operates versatile ships that may carry each, bulk cargo in addition to tanker cargo. The 380 mn EUR market cap firm has been IPOed in 202 and has completed fairly nicely, as a number of different delivery IPOs. The ships look spectacular however in any other case fairly regular:

The corporate claims that their vessels are extra gasoline environment friendly which might make it fascinating for clinets concerned with low CO2 transport.

The inventory trades at 6x 2022 earnings which seems to be low cost, nonetheless margins in 2022 have been a minimum of 2x of historic ranges. The corporate is kind of optimistic for 2023. Ships are to me equally international like actual property, so I’ll “cross”.

77. Inin Group AS

Inin is a 26 mn EUR market cap Holdco that made losses for a few years. After their IPO in 2020, they offered their fundamental enterprise in 2022, renamed themselves from Elop into Inin and have purchased a number of new companies targeted on contruction and inspection of infrastructure. Sounds good in precept however seems to be sketchy from the numbers.

The corporate has been and might be loss making however desires to turn out to be “Money circulation optimistic” in 2023. “Move”.

78. Ensurge Micropower

Becoming to the title, Ensurge is a 5 mn EUR market cap Micro Cap claims to develop Soldi State battery and has simply issued new shares. “Move”.

79. Hyon

Hyon is a 3 mn EUR nanocap that tries to revolutionize one thing within the Maritime Hydrogen ecosystem, I’m not actually positive what. They IPOed in early 2022 and the share worth since then went solely down. They’ve some gross sales however general this firm appears to be too small and early to be fascinating. “Move”.

80. Orkla

Orkla is a 6.4 bn EUR market cap firm that “is a number one provider of branded shopper items to the patron, out-of-home and bakery markets within the Nordics, Baltics and chosen markets in Central Europe and India. Branded Shopper Items contains Orkla Meals, Orkla Confectionery & Snacks, Orkla Care, Orkla Meals Substances and Orkla Shopper Investments”.

The long run chart doesn’t help a variety of worth creation over time:

Nevertheless, trying on the fundamentals, it’s fascinating to see that there was respectable progress within the final years and that the inventory trades at a relatviely low cost degree in comparison with its previous at 13,6x P/E and 12 x EV/EBIT. In 2022 the meals division strugged a bit of bit, nonetheless additionally they have a Hydropower division extra then offset that. In addition they promote meals merchandise in India on high of their Nordics focus. General Orkla appears to be a really various firm and a really fascinating “animal” that I’d need to be taught extra about. “Watch”.

81. Storebrand

Storebrand is a 3,6 bn EUR monetary firm that’s principally energetic in life insurance coverage and long run financial savings merchandise. the long run chart we will see that there isn’t any huge long run worth creation however that the inventory is apparently buying and selling close to ATH ranges:

That is suprising as at fisrt sight, 2022 reslts have been considerably under 2021. Nevertheless the corporate introduced an honest dividend and a share purchase again program. They’ve really comitted to purchase again 10 bn NOK in shares till 2030. However, I see only a few causes to personal a Norwegian Life insurer, subsequently I’ll “cross”.

82. Statt Torsk

Statt Torsk is a 29 mn EUR market cap fish farmer that for a change is farming Cod as an alternative of the same old Salmon. The corporate IPOed in early 2021 and has misplaced -50% since IPO. They really have gross sales however little or no and are loss making because the fish are principally within the rising part. Though I choose Cod to Salmon on my plate, I’ll “cross” on that.

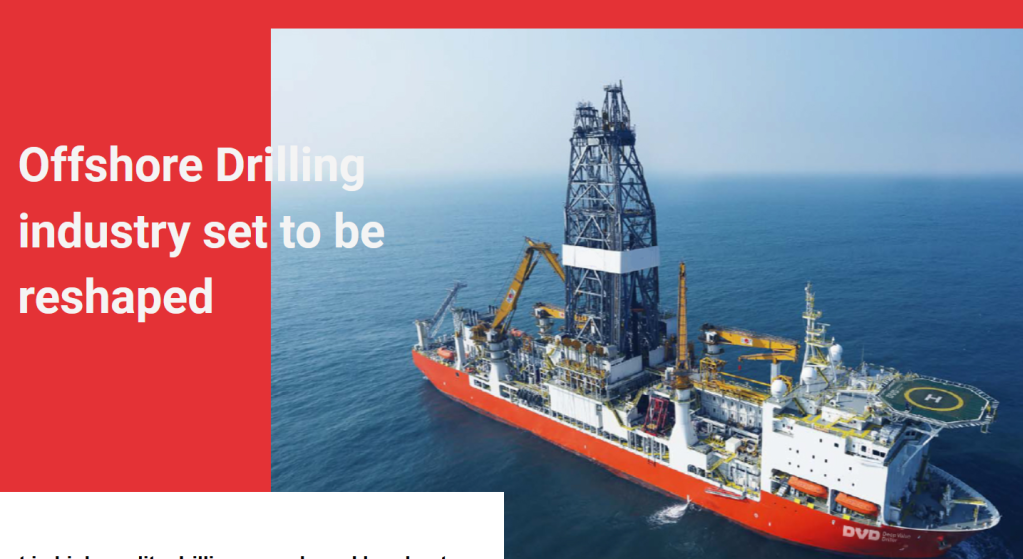

83. Deep Worth Drilling

Regardless of having an ideal title for any Deep Worth Investor, this153 mn EUR market cap owns a single drillship and rents it out to drilling corporations. IPOed in 20221, the inventory has greater than doubled. In accordance with their firm presentation, the bough the ship for 65 mn USD in comparison with the fee to construct it of 750 mn USD. That is what they received (I like to pst ship photos):

Nevertheless, cool ships don’t essentially make nice long run investments, therfore I’ll “cross”.

84. Havila Kystruten

Havila is a 71 mn EUR market cap and operates 4 cruise ships that run the Fjord tour between Begen and Kyrkenes. The corporate was IPOed in 2021 and has completed actually dangerous and has misplaced greater than -50% for the reason that IPO. Earlier than shortly passing this nonetheless, I noticed that one in all my “friends”, Paladin owns 6,7% of the corporate and I kjnow that they’ve invested efficiently in Norwegian Ferry corporations earlier than. Once more right here an image of one in all their ships:

The corporate appears to be within the construct up part and made losses up to now, additionally as a result of LNG gasoline was very costly. In any case, due to the Paladin guys, I’ll “watch” this one.

85. Kraft Financial institution

Kraft Financial institution is a 33 mn EUR market cap Financial institution that “provides refinancing of mortgages and unsecured loans to people that attributable to a difficult private financial system and/or difficult liquidity can’t refinance at an everyday financial institution.”. So one thing like a “subprime” participant.

The Financial institution is kind of younger and has grown quick. ROE’s reched 12-13% in 2021 and 2022. At 8x P/E it seems to be low cost.

Most of their studies are in Norwegian, however I actually discover this one fascinating. “Watch”.

86. Petronor E&P

Petronor is a 116 mn EUR market cap oil explorer that’s energetic in very unique places like Congo and Senegal. Not my cup of tea and since its IPO in 2022, the inventory worth did little or no. “Move”.

87. EAM Photo voltaic

EAm Photo voltaic is a 3 mn EUR market cap firm that operates photo voltaic crops in Italy or inittially deliberate to take action. There appears to be a really particular story that they’ve been cheated on their preliminary buy in 2014 and are actually principally litigating in Italy. That is how they describe themselves within the 2021 report: “This case has successfully modified EAM from a YieldCo to a big listed lawsuit”. Not my form of particular state of affairs, “cross”.

88. TECO 2030

TECO is 145 mn EUR market cap firm that does develops Hydrogen gasoline cells for the delivery trade. The corporate has little income and regardless of capitalizing a variety of bills, is making massive losses. Curiously, aside from many comparable cleantech start-ups, the inventory is up 2,5x from its 202 IPO. “Move”.

89. Ocean Solar

Ocean Solar is a 30 mn EUR market cap “floating PV” firm that “has developed an revolutionary answer to international power wants. The patented expertise relies on photo voltaic modules mounted on hydro-elastic membranes and provides value and efficiency advantages unseen in every other floating PV system immediately”.

As one other 2020 IPO, the share worth intitally took off like a rocket however now trades at lower than 1/2 of the IPO worth. They do have some slaes and have realized some demonstration initiatives. Right here is an instance:

They appear to have money left for 2-3 years on the present burn charge. With a view to have a minimum of a number of of the Norwegian Clear techs on the watchlist, they get a (weakish) “watch”.

90. Awilco LNG

Awilco is a 110 mn EUR market cap firm that owns 2 LNG carriers. After a number of very dangerous years, issues appear to look higher. This could possibly be in principle an fascinating hypothesis on LNG imports within the subsequent years. Their ships seem like being GTT designs:

However, I’ll attempt to keep away from ships, subsequently I’ll “cross”.

{kind=link}