Mortgage Q&A: “What time of yr are mortgage charges lowest?”

We’re all on the lookout for an angle, particularly if it’ll save us some cash. Whether or not it’s a inventory market development, a house worth development, or a mortgage fee development, somebody at all times claims to have unlocked the code.

Sadly, it’s often all nonsense, or predicated on the idea that what occurred up to now will happen once more sooner or later.

Generally historical past repeats itself, typically it doesn’t. We most likely solely hear concerning the occasions when it does as a result of it makes the person behind it sound like a genius.

Now in the event you’re questioning if there’s a “greatest time of yr to get a mortgage,” the reply is there might be. And positively higher (and worse) occasions than others.

What Time of Yr Are Mortgage Charges the Lowest?

In actuality, it’s very troublesome to foretell something, even the climate, so in the case of complicated stuff like mortgage rates of interest, success charges most likely transfer quite a bit decrease.

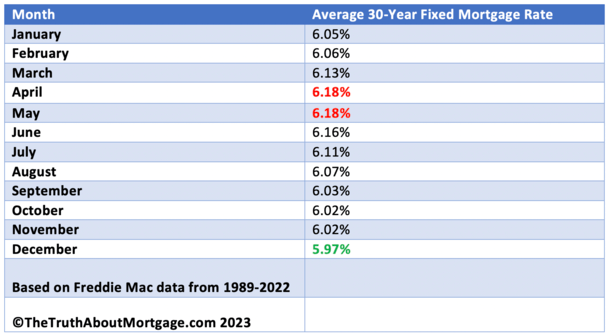

That being stated, I got down to see if there have been any mortgage fee developments we may glean from accessible knowledge, utilizing Freddie Mac’s historic mortgage charges that return to 1971.

With 50 years of information at our fingertips, you’ll suppose some developments would seem, proper?

Had been mortgage charges decrease in sure months, larger throughout others, or is all of it simply random? Let’s discover out.

For the file, I checked out month-to-month averages for the 30-year fixed-rate mortgage over the previous three a long time to find out if there’s a profitable month on the market.

I omitted the way-back years (just like the 70s and early 80s) as a result of mortgage charges weren’t on the identical stage as they’re these days.

The desk above lists common mortgage charges by month. It has been freshly up to date utilizing knowledge from 2021 and 2022 to offer probably the most present outcomes.

Maybe You Ought to Store for a Mortgage As an alternative of Vacation Items…

It seems there’s a month when mortgage charges are lowest. And as you could count on, it’s at a time when most folk wouldn’t even be fascinated about buying a house or refinancing an current mortgage.

Sure, it’s December. You realize, when people are extra involved with vacation procuring and touring to see household then calling up a mortgage lender.

Or when it’s a lot too chilly to even take into consideration doing something tremendous work-intensive like filling out a house mortgage utility.

This might clarify why mortgage charges are lowest in December. In the event you recall, lenders go on larger reductions to shoppers when issues are gradual.

And December is at all times going to be a gradual month for mortgage lenders, which most likely has one thing to do with the low cost seen over the previous 30 years.

It’s not big, however a mortgage fee 0.25% decrease may end up in massive financial savings over time.

Preserve an Eye Out for a Mortgage Price Sale All through the Yr

- Mortgage lenders function similar to different sorts of companies promoting merchandise or items

- They worth their loans primarily based on anticipated revenue margin and operational prices

- If their enterprise slows down they is perhaps inclined to decrease the value (or rate of interest)

- But when they’re doing a variety of enterprise (and even too busy) they may hold charges artificially excessive

Much like some other firm on the market promoting items, there are “gross sales” at sure occasions all year long, and in addition occasions when costs are marked up.

As you would possibly count on, if an organization is attempting to maneuver product, on this case residence loans, what do they do? They decrease the value to drive enterprise.

Mortgage lenders capable of decrease the value, or fee, as a result of they’ve received a margin in-built to their market fee.

This margin acts as their revenue, minus operational prices. Certain,they might not make as a lot per mortgage in the event that they decrease charges for shoppers, however they may make up for it on quantity.

As an alternative of closing one higher-priced mortgage, they is perhaps comfortable to shut three loans and earn extra on mixture. So that they have wiggle room to play with charges a bit.

They will modify them decrease when enterprise is crawling, and easily keep or elevate them when their telephone received’t cease ringing.

How A lot Cheaper Can Charges Actually Be in a Given Month?

- Mortgage charges are measured in eighths of a p.c (0.125%)

- Which can look or sound like completely nothing when evaluating charges

- However that small distinction might be exponential since you pay the mortgage every month for years (presumably 30!)

- This explains why even a marginal distinction in fee can quantity of hundreds of {dollars} over time

Okay, so we all know charges differ all year long, and even a small distinction in fee might be very significant. However how a lot can you actually save?

Whereas not huge by any stretch, you would possibly have the ability to get a fee .25% decrease in December versus April. Identical goes for October and November in comparison with spring.

If we’re speaking a couple of $300,000 mortgage quantity, a fee of 6% vs. 6.25% is the distinction of roughly $50 monthly, or almost $600 per yr.

Preserve your mortgage for a decade and also you’ll pay almost $5,000 extra over that interval.

Are You Overpaying for Your Residence Mortgage and Home in April?

- The most typical time to purchase a house is in spring, often the month of April

- That is when most potential patrons get critical and make presents

- It’s additionally when extra residence sellers lastly determine to record their properties

- Nevertheless it is perhaps cheaper to purchase a house throughout fall or winter when issues are gradual

Now talking of April, that month tends to be prime time for residence shopping for traditionally, which explains the shortage of a reduction.

The identical goes for purchasing a house throughout April – it’s quite a bit much less frequent to see a worth discount throughout spring than it’s throughout fall or winter.

All of it begs the query; ought to we purchase properties when costs, competitors, and rates of interest are lowest? In all probability.

Only one drawback – there tends to be much less accessible stock within the fall and winter months as effectively. However in the event you do come throughout one thing you want, it might be a good time to snag a deal.

In different phrases, it’s best to at all times be wanting, even when it’s not the best time to maneuver.

In the event you’re refinancing a mortgage, there are much less obstacles in December because you’ve already received a home.

To sweeten the deal, lenders most likely aren’t busy, so that you’ll breeze via underwriting quite a bit faster. And you might obtain a little bit extra consideration out of your mortgage officer.

Ought to I Wait Till December to Get a Mortgage?

In brief, most likely not. Whereas December had the bottom mortgage charges on common over the previous 30 years, there have been loads of years when charges have been larger in December in comparison with different months.

Take 2018, the place the 30-year fastened averaged 4.03% in January and 4.64% in December.

Identical goes for 2015 and 2016, when charges have been markedly larger in December versus the start of the yr.

Final yr was additionally a foul December, with the 30-year fastened averaging 3.45% in January and 6.36% in December.

Nevertheless, in 2020 the 30-year fastened averaged 3.31% in April and a pair of.68% in December, which is a distinction of 0.63%. That may equate to hundreds of {dollars} in financial savings.

All in all, you’re most likely higher off being attentive to what’s happening in financial system if you wish to predict the path of mortgage charges.

The development (transferring up or down over a time period) is perhaps extra vital than the month of yr.

Merely put, unhealthy financial information usually results in decrease mortgage charges, whereas optimistic information tends to propel rates of interest larger.

Time of yr apart, you would possibly have the ability to save much more in your mortgage just by gathering quotes from multiple lender.

In the end, timing doesn’t appear to be the most important driver of charges, neither is it one thing most of us can management anyway.

(picture: Marco Verch)

{kind=link}