Background:

Again within the good previous days (2018) when Enterprise and Development investing have been nonetheless attractive, I seemed into the world of “listed Enterprise Capital”:

Half 1: HOW TO INVEST INTO VENTURE CAPITAL – LISTED VEHICLES (PART 1)

Half 2: HOW TO INVEST INTO VENTURE CAPITAL PART 2: AUGMENTUM, VOSTOK & OTHERS

Inititally I purchased into Kinnevik, Vostok New Ventures (renamed to VNV) and Vostok Rising Finance (now VEF), nevertheless, I offered each Kinnevik and later VNV (at smallish earnings) and solely held onto VEF. That is how the Group has carried out since then (november 2018) (Costs in native foreign money solely, no dividends/Spin-offs):

Sadly I couldn’t discover steady comparability charts for VNV and VEF, however nearly all the shares at first struggled in 2019, solely to go bonkers in late 2021 after which crumble in 2022.

Initially I cursed myself for promoting too early , however now it seems tremendous good to solely hold one that could be a “winner”.

The story of the 2 “Vostoks”: Why so totally different ?

After I seemed on the two Vostok Autos again then, each nonetheless had a major Russia publicity which they nevertheless managed to get rid off at good valuations earlier than the present points.

The query remains to be: Why has the efficiency differed a lot although the businesses have the identical roots ? Per Brilioth, the CEO of VNV is definitely nonetheless a board member of VEF.

One facet that I had noticed again them after I was in a position to converse with each of them was, that VNV was extra aggressive in threat taking than VEF. That is for example the 2019 Portfolio of VNV:

We are able to see that they’d shifted largely into Mobility and Digital well being by that point and that they really had web debt of virtually 10% of NAV. When then Covid hit and particularly their mobility holdings bought into hassle, they needed to concern shares at ~55 SEKs (together with a warrant).

In addtion, VNV “ventured” from their unique core space of “Market locations” into moblity and digital well being which they recognized as international mega tendencies.

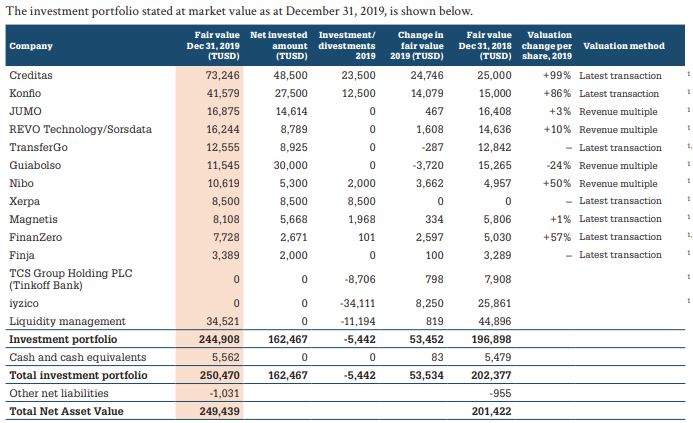

VEF compared by the tip of 2019 nonetheless had ~15% of its NAV in money or money equivalents:

Quick ahead to 09/2022 and we will see that for VEF, the large winner was (and nonetheless is regardless of a -50% “haircut”) the Brazilian Fintech Creditas:

Additionally their second largest Funding, Konfio has executed properly. VEF has nonetheless web money however clearly lower than in 2019. They’ve been issuing debt and hold shopping for again shares which clearly makes the assemble a lot riskier.

Taking a look at VNV, we will see that they nonetheless run a web debt place:

We are able to additionally see that their 2019 prime positions have all been “smoked”. Particularly Babylon, which in some unspecified time in the future had been the most important place has misplaced greater than 95% after its IPO. What was purported to be a “constructive liquidity occasion” become a nightmare.

What can be attention-grabbing is that the three remaining largest positions of VNV are Mobility firms. Particularly for VOI, the Scooter firm, many individuals assume that the valuation may not make sense. Listed competitor Chicken is buying and selling at an Enterprise Worth of 100 mn USD, due to this fact assuming a 6x larger valuation for VOI is clearly a stretch. Gett had deserted a SPAC IPO in March 2022, as a listed firm, their worth would clearly not be near 1 billion. It is usually attention-grabbing that VNV invested a full 48 mn into Gett this yr.

One other bombed IPO was Center East mobility firm Swvl which managed to lose an astonishing -99,85% since their SPAC IPO. On the finish of 2021, VNV had the inevstment with greater than 100 mn USD on their books.

With regard to Babylon, I had all the time doubts. Again then I had really the chance to get some perception into Babylon and the corporate all the time seemed like “too good to be true” to me. They made plenty of claims on their expertise nevertheless it was by no means clear what was really there and what was solely a modern animation.

Lastly, their unique market place investments appear to have executed moderately properly and allowed them some respectable exits, reminiscent of Hemnet. That is clearly Hindsight bias, however sticking to market place enterprise fashions would have been clearly higher.

Exterior in assessement on VEF vs VNV:

It’s all the time troublesome from to evaluate the efficiency from the surface, nevertheless the next observations are perhaps legitimate:

- VNV was all the time extra agressive by using web debt which then required them to concern new shares at a depressed value whereas VEF was/is ready to purchase again shares.

- Whereas VEF caught to their Fintech core, VNV diversified into Mobility and and Digitgal Well being which turned out to be problematic

- VNV retains investing in present even when issues go south. That’s ususally not a very good technique in VC. One ought to make investments into the winners and let the losers go down

- Lastly, the truth that Covid negatively impacted particularly mobility investments may also be attributed to plain dangerous luck.

General, regardless of the big “low cost”, I don’t assume that VNV is a should have funding. A lot of their holdings are “structurally” challenged. I nonetheless would favor VEF over VNV.

VEF for me is a comparatively small wager. Intitally I deliberate to extend the place over time, however in the meanwhile I’ll watch how issues develop.

UK Enterprise Capital Trusts

In my preliminary 2 posts I fully forgot a couple of comparatively established “asset class” that exists within the UK: Closed finish Enterprise Capital Trusts. Right here is an Investopedia submit that explains the fundamentals.

Citywire has an inventory of 39 of those autos. As well as, a few these funds additionally run Plc’s that make investments into Enterprise Capital reminiscent of Molten Ventures. These autos appear to have very “related” reductions in comparison with the opposite listed firms an that house.

Per 30.09. Molten Ventures for example reported a NAV of 837 Pence per share vs. a share value of ~300 Pence. Once more the Efficiency in comparison with November 2018 can be not nice:

Their funding portfolio is a mix of direct investments and funds. The reporting is much less clear than for isnatnce Vorstok. For some purpose for example, they don’t disclose % possession stakes of their direct holdings and there may be little or no information on the “fund of fund” half which is 1/3 of gross portfolio worth.

One other listed Car is Chrysalis Investments Plc. I frst heard about them when pip_net from the Doppelgaenger Podcast shorted them due to their Klarna publicity.

Chrysalis reported a 30.09.2022 NAV of 147 Pence vs. a shareprice of ~60 pence, the same “low cost” in comparison with Molten. The most important place of Chyrsalis is Wefox, a German “Insurtech” that in my view has alos a fairly uncertain bsuiness mannequin.

Taking a look at each, Molten Enterprise and Chrysalis, we will additionally see that over the past 5 years, they each carried out worse than the FTSE 100 which itself was not an awesome performer:

Perhaps 5 years is simply too brief nevertheless it seems like that listed Enterprise Capital as such doesn’t appear to be the large residence run that many individuals believed it to be. Apparently there are nonetheless plenty of efforts to “democratize” Enterprise Capital however total it seems like that every time Enterprise Capital finds its method to the general public, one of the best days are over.

My intestine feeling is that we’re nonetheless too early within the cycle to go for “cut price looking”, if in any respect.

Abstract:

I do assume that the monitor document over the previous 4 years of public Enterprise capital is at greatest “combined”. Many autos have created solely restricted worth, in the event that they created worth in any respect.

Will probably be attention-grabbing to see how markets react if we certainly see an extended “VC winter” in comparison with the very temporary disruption throughout Covid.

Perhaps it might make sense to take a look at the sector in a single years time once more to see if there are some “actual” bargains, in the intervening time I’d not be so positive. The perceived reductions may to a big lengthen be inly timing delays earlier than the valuations of the underlying investments get marked down considerably within the coming months and years.

General, I don’t assume that “Public Enterprise” is a really helpful assemble because it appears to be plenty of “adversarial choice”, i.e. the actually good offers go to the highest funds that don’t must trouble round with reatil cash. So I’ll abstain from making extra investments into such autos until there’s a clear cut price/particular scenario.

{kind=link}