.png#keepProtocol)

Purchasing round and switching has fallen notably because the value strolling ban.

With an industry-wide regulator-enforced assure that renewing clients wouldn’t be charged greater than if they’d been a brand new buyer.

Within the residence market, 76.1% of consumers shopped round in April-June 2019, dropping to 71.5% in April-June 2022. Switching fell from 37.1% to 34.7%.

In the meantime within the motor market, procuring dropped from 83.1% to 79.4%, and switching from 39.7% to 36.9% in the identical three-year interval.

However with the cost-of-living disaster biting more durable, customers could effectively discover and realise that there are financial savings available, even when their renewal quote hasn’t jumped up.

So what’s at the moment motivating procuring and switching behaviour – and what can suppliers study from it forward of the anticipated spending crunch?

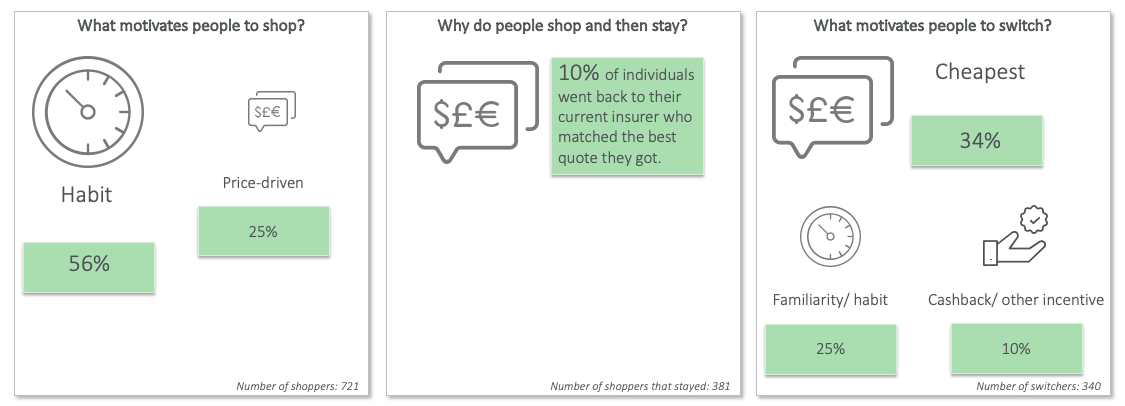

Residence insurance coverage procuring and switching

In Residence, it’s attention-grabbing to see that solely 25% of consumers are at the moment pushed by value. 56% store out of behavior – having been educated over a few years that go (dot) evaluating the market is the easiest way to get the most effective deal.

Some 10% of these consumers selected to stick with their present supplier after seeing what else was on the market.

Of those who do swap, solely 34% had been motivated by the most affordable value, and solely 10% by incentives like cashbacks. 1 / 4 are switching primarily out of behavior.

Motor insurance coverage swapping and switching

In Motor insurance coverage, barely extra consumers had been value pushed – 14% as a result of their quote had gone up loads at renewal and 13% who needed to make use of a quote to renegotiate with their present insurer. An extra 56% stated they store round every year on precept.

Motor clients are way more motivated to truly make the swap by the most affordable value – with 50% citing it as their predominant motive for altering suppliers.

The place now?

Because the rising value of residing takes maintain and clients start to really feel the pinch, we’re anticipating to see procuring charges enhance. The massive query is whether or not switching charges will go up, and that may solely occur if clients really feel as if they’re saving cash by switching.

With cash being a giant motivating issue already – particularly in motor – it’s probably individuals will probably be keener for a deal.

This implies new new-business alternatives – however there are additionally alternatives to extend the variety of consumers who select to remain after trying round. Sure, value goes to be necessary, however it’s clearly not the one entrance on which to struggle for them. Communication will probably be completely key – particularly for purchasers thrown into monetary vulnerability, and on the level of a grudge expenditure. How can they be made to really feel protected and valued? Will perks immediately begin to imply extra – or much less as individuals minimize down on journeys to the cinema and eating places?

What we have to be positive of is that the proliferation of decrease worth insurance coverage merchandise we’ve seen getting into the market doesn’t imply that saving cash leads to compromising cowl.

Suppliers have a duty to offer, and articulate, truthful worth. These in a position to take action could be the ones who show hottest with cost-of-living consumers and switchers.

[September Report] Value of Dwelling Client Behaviour Tracker

With our ‘Value of Dwelling’ Client Behaviour Tracker, you possibly can observe altering sentiment, attitudes, and behaviours, as customers proceed to face the rising value of residing.

Touch upon weblog put up . . .

.png#keepProtocol&description=How%20is%20the%20cost-of-living%20disaster%20impacting%20procuring%20and%20switching%3F){kind=link}