A credit score rating is a numerical illustration of the chance of you defaulting on a mortgage. It ranges from 300 to 850. The upper the quantity, the much less seemingly you might be to default.

Credit score scores are supplied by two corporations: FICO® and VantageScore. These corporations base their scores on info in your credit score stories from the three main credit score bureaus: Experian, Equifax and TransUnion. They run this info via proprietary algorithms to supply your rating.

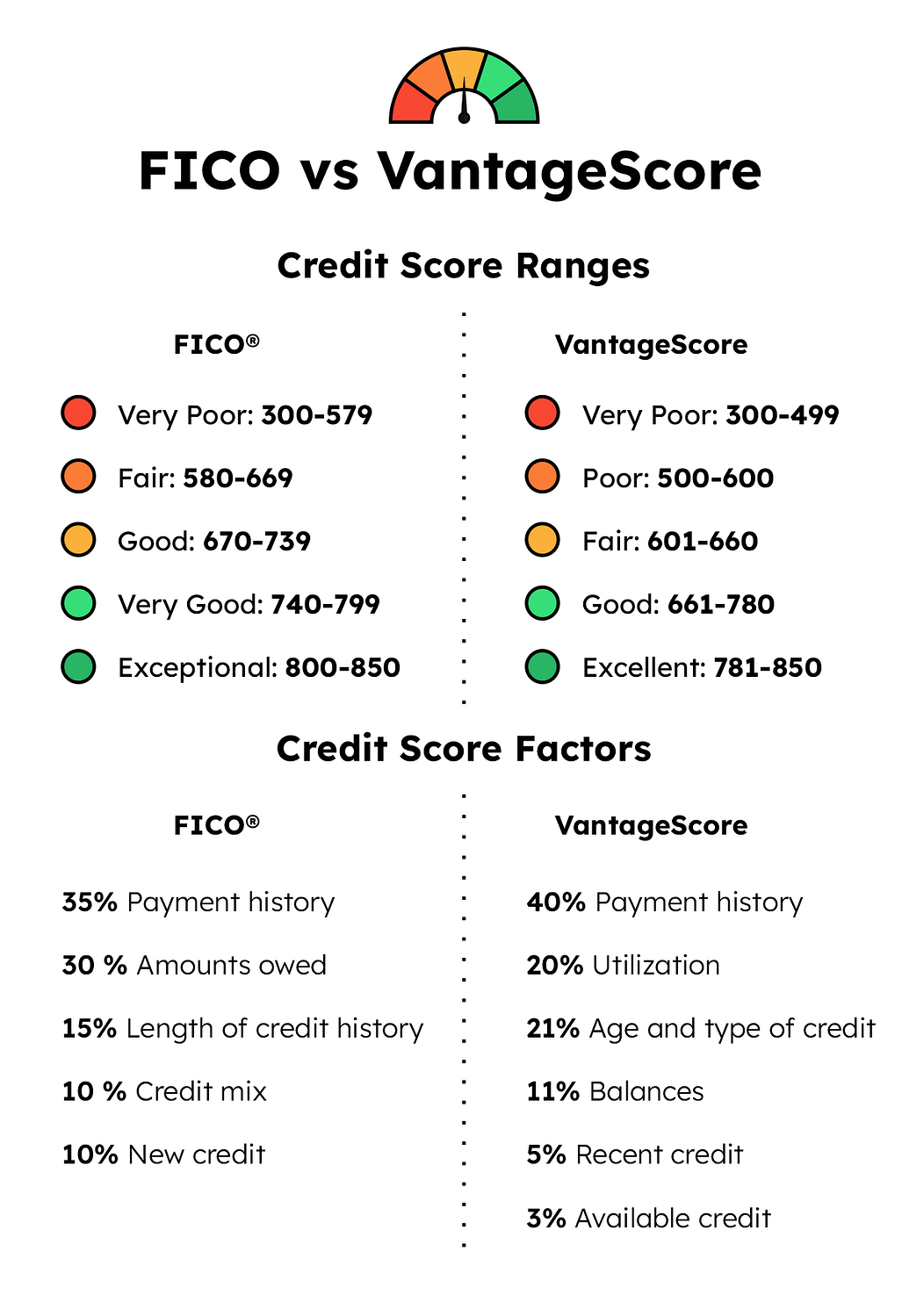

Let’s check out what represent an excellent FICO rating in addition to what an excellent VantageScore may be.

What Is A Good FICO Rating?

“FICO” stands for Honest Isaac Corp., the primary firm to develop a broadly used numerical credit standing scheme.

FICO classifies any rating between 670 and 739 as “good”. Scores between 580 and 669 are thought to be “truthful,” whereas 740 and 799 are thought to be excellent. Something above 800 is taken into account “distinctive.”

What Is A Good Ranking With VantageScore?

FICO competitor VantageScore generates the same ranking utilizing the identical credit score stories. The VantageScore algorithm is totally different, so the scores is not going to be the identical as FICO scores.

VantageScore classifies scores from 661 to 780 as “good”. VantageScores 780 to 850 are thought of “distinctive”, whereas these between 601 and 660 are “truthful.” VantageScores decrease than 600 are thought of “poor.”

How Many People Have a Good Credit score Rating?

The typical American Fico rating in April 2022 was 716, which is squarely within the “good” vary. Right here’s how the scores break down:

67% of People with credit score scores have good, excellent, or wonderful credit score. Solely 33% have truthful or poor credit score. These percentages don’t embrace the 45 million adults who haven’t any credit score rating!

What Will a Good Credit score Rating Get Me?

The rating ranges we mentioned above are set by FICO and VantageScore. Particular person lenders might use totally different ranges. For instance, lenders making secured loans, like mortgages and automobile loans, might settle for decrease scores as a result of the mortgage is protected by collateral.

A rating that’s “good” to FICO or VantageScore is probably not in the identical class for any given lender. Nonetheless, as a normal rule, you’ll be able to count on to get accredited for many loans and bank cards with a “good” rating, particularly for those who’re within the higher a part of the “good” vary.

Whereas you’ll get accredited, you might not get the bottom charges ot the very best phrases, that are reserved for debtors within the “excellent” and “wonderful” ranges. You is probably not accredited for premium merchandise, just like the bank cards with the best rewards.

If you happen to intention for perfection, you need to know that only one.3% of debtors have an ideal credit score rating. Happily, it doesn’t matter a lot[1]. An 800 rating will get you a similar offers as an 850 credit score rating.

When you’re within the “wonderful” vary, lenders and card issuers will roll out the crimson carpet!

Most lenders shall be very pleased with an 800 credit score rating, however the dimension of the mortgage they may provide is not going to simply rely in your credit score rating.

The scale of the mortgage you’re supplied can even rely in your revenue, belongings, and debt-to-income ratio. Lenders making secured loans will lend greater than lenders making unsecured loans.

Your 800 rating makes it simpler to get a mortgage however doesn’t decide the dimensions of that mortgage.

A 700 credit score rating is within the “good” vary however beneath the US common. You’ll qualify for loans and bank cards, however you gained’t get the very best rates of interest or phrases, and you might not qualify for premium merchandise.

If you happen to’re contemplating a significant mortgage, like a mortgage or automobile mortgage, it’s value working in your credit score rating first. Even a modest improve may prevent 1000’s of {dollars} over the lifetime of the mortgage.

You will get loans and bank cards with a 650 credit score rating, however don’t count on the very best rates of interest, and be ready to doc an excellent revenue and an appropriate debt-to-income ratio.

You’ll have to store for lenders who will take into account a 650 rating as a result of not all do. Perform some research on minimal credit score scores earlier than you apply. You don’t wish to apply for loans you aren’t going to get!

Credit score Scoring Elements

Quite a few components are used to calculate your credit score rating. Though the precise standards utilized by every ranking mannequin range, the next are a very powerful influences in your FICO rating.

- Cost Historical past: on-time funds are the only most necessary a part of your credit score rating.

- Credit score Utilization: credit score utilization is the proportion of your credit score restrict that you’re utilizing in your revolving accounts, like bank cards.

- Size of Credit score Historical past: primarily based on the common age of your energetic credit score accounts.

- New Credit score: every time you apply for credit score, a tough inquiry is positioned in your account.

- Credit score Combine: your credit score combine is the stability between installment credit score and revolving credit score.

VantageScore makes use of very related standards, although they’re weighted in a different way.

Understanding how your credit score rating is calculated is a crucial step towards enhancing it.

⚠️ Tip: Tax liens, civil judgments, alimony, and youngster assist obligations don’t seem in credit score stories. Nevertheless, lenders can find them via public data, and they’re going to have an effect on your capacity to get credit score.

The Advantages of a Good Credit score Rating

Your credit score rating is designed to measure the chance that you’ll default in your mortgage obligations. It’s used for a lot of functions exterior of lending, although. Listed below are among the advantages of an excellent credit score rating:

- Simpler qualification. Everytime you apply for a mortgage, bank card, or every other kind of credit score, the lender will confirm your credit score rating. Good scores make it simpler to qualify.

- Higher rates of interest. Lenders provide decrease charges to low-risk debtors. The financial savings could be vital.

- Higher entry to employment. Some employers will confirm your credit score rating earlier than making a hiring choice.

- Renting will get simpler. Landlords will test your credit score earlier than renting you a home or residence.

- Keep away from Costly Varieties of Credit score. If you happen to can’t get accredited for loans or bank cards, you may need to make use of expensive types of credit score, similar to payday loans, to cowl a deficit.

Consider your credit score rating as a monetary report card. A passing grade makes your total monetary life simpler!

How To Enhance Your Credit score Rating

You possibly can enhance your credit score rating. Listed below are some methods to start out:

- Get a free copy of your credit score report. Understanding what’s in your credit score report may also help you study what helps or hurting your rating.

- Dispute inaccurate info in your report. Your scores might endure as a result of incorrect info in your credit score file. If you happen to see inaccurate info in your credit score report, dispute it without delay.

- Make any excellent funds. Late funds and delinquent accounts are credit score rating kryptonite. Get your funds present and hold them that means!

- Set Up Extra Frequent Funds. Making funds a number of instances a month will provide help to hold your stability down and decrease your credit score utilization ratio.

There are lots of different methods to construct credit score, however the simplest are probably the most fundamental: make your funds on time and hold your bank card balances low!

⚠️ Tip: Don’t shut any bank cards you’ve gotten paid off. Closing accounts raises your credit score utilization ratio and shortens the common age of your credit score accounts.

FAQ

Paying payments on time is the only largest contributor to an excellent rating. Being behind on any cost for any size of time will damage your rating badly.

You’ve many credit score scores. Your credit score scores could also be totally different if the data is sourced from totally different credit score bureaus. Credit score rating suppliers additionally present specialised credit score scores for particular makes use of, like auto loans and bank cards.

All of those scores are primarily based on info in your credit score stories, however the info could also be processed in a different way or sourced from totally different credit score bureaus.

Credit score scores are calculated by credit score scoring corporations, primarily FICO and VantageScore. They’re primarily based on info in credit score stories collected by the three main credit score bureaus: Experian, Equifax, and TransUnion.

Opposite to standard perception, your rating doesn’t start at 300. You begin out with no rating in any respect: when you’ve got no credit score report or only a few data, you’ll not be thought of scorable. If you happen to make common funds on a number of loans or bank cards, you’ll accumulate a decent rating of roughly 700 simply inside just a few months.

Most medical organizations don’t report back to credit score bureaus. Nevertheless, if an account is offered to a set company otherwise you use bank cards to pay medical payments, you’ll be able to damage your credit score rating.

The reply was once “no”, however two providers can now provide help to embrace invoice funds for credit score bureaus. Join with Experian BOOST™ or eCredable Elevate. This may enhance your rating by as much as 15 factors. Not all scoring fashions will embrace this info.

{kind=link}